Better Days Ahead At Monro, Inc?

Margins and revenues at the tire-replacement chain may be set to recover.

Wearing Thin

To borrow a well worn phrase from Wayne Gretzky, the best investments in our view are the ones in which investors skate to where the puck is going, rather than to where it currently is. In other words, investment opportunities can often be found in places where most investors or analysts are discouraged but where there is reason to believe that sentiment is likely to change in the future. Today, we focus on just such a company—Monro, Inc (symbol MNRO).

With roughly 1,300 locations across the United States and a $1 billion market capitalization, Monro is a leading provider of tires and auto repair. Monro describes its business as such:

[R]eplacement tires and tire related services, automotive undercar repair services, and a broad range of routine maintenance services, primarily on passenger cars, light trucks, and vans. We also provide other products and services for brakes; mufflers and exhaust systems; and steering, drive train, suspension, and wheel alignment.

The stock has suffered across multiple time frames. On a five year basis it has fallen 48%, 22% over three years, and 31% in the last twelve months. The primary reason for this, as readers may suspect, is lackluster revenue growth.

On revenues of $327 million in the latest quarter (roughly the company’s pre-pandemic revenue), Monro generated $17 million in operating income.

At the start of 2023, the company decided to not issue annual guidance—never a good sign. The few analysts which cover the stock have a lukewarm outlook as well, with average price targets at $37.50 (as of this writing the stock trades at $33).

Looking under the hood reveals why Monro has suffered as of late. Speaking at the UBS Global Consumer & Retail Conference, CFO Brian D'Ambrosia gave a high-level on Monro’s customer base:

[Monro’s customer] may be a single-person household driving, making $50,000 or less, driving [their vehicle] for obvious economic reasons and affordability issues of new vehicles as they look at their overall spend across their categories. And it's the same thing for households $100,000 or lower that are doing that as well. We'll also see some more affluent households that have maybe 2 or 3 free vehicles, the third vehicle may be for a daughter or a son and those create that third vehicle that's aged. And they're likely the customer of both the dealer for their newer vehicles and of the aftermarket.

The typical car Monro services is 6-12 years old, what D’Ambrosia calls the company’s “sweet spot.”

It isn’t difficult to see the issue here—Monro’s core customer has been under pressure from inflation over the last 18 months. Let’s take a look at Monro’s revenue mix from June 2023 compared to pre-Covid numbers from June 2019.

We can broadly break out Monro’s business into two segments—tires and service (management discusses the business along the same lines). Tires are big-ticket and require a large amount of cash up front for Monro when compared to services (brakes, undercarriage servicing, etc), which are cash-light in terms of inventory but are more labor intensive. The tire business tends to be lower margin than services overall, but service margin has also likely been under pressure due to a tight labor market.

Key Drivers

Make no mistake—Monro’s business is commodity-driven. The only competitive advantage Monro may have in the aftermarket marketplace is its scale as a player, but not much more than that. Given this, the key drivers for the business are, in our view, total miles driven by customers, and key input costs such as rubber and shipping.

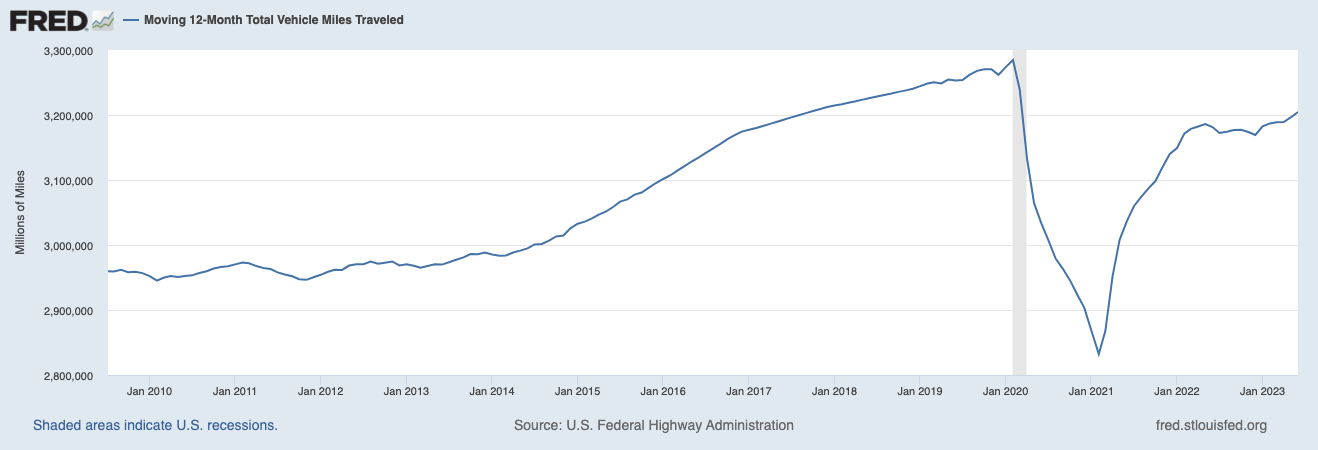

Total miles driven seems like an obvious place to start—the more people drive, the faster tires wear out. According to a Federal Reserve Bank of St Louis study, August-September are generally the months in which Americans tend to drive the most.

Total miles traveled by Americans are also up (see chart above), though according to data from the Federal Highway Administration the pre-covid peak of miles driven has not yet been surpassed. The trend, however, has resumed its up-and-to-the-right dynamic and according to a survey from the Vacationer, Americans have planned an estimated 100 million road trips of more than 150 miles in 2023.

Rubber prices have also normalized from their peak during the great Supply Chain Bottleneck of 2020-2022.

While rubber is only a component of modern pneumatic tires, its cost is a key proxy in estimating the cost of Monro’s largest cost input. After jumping to over $1.00 per pound in 2021 and flirting with $1.00 again in 2022, prices have subsequently fallen to just under $0.70 per pound today.

Similarly, shipping costs eat into Monro’s margins as the vast majority of tires are shipped to the United States from overseas.

The Baltic Dry Freight Index (pictured above with a 10-year view), which measures the average cost for a shipping container, has fallen to below its ten-year average of $1,356 to $1,223 as of this writing.

Lastly, while not necessarily a key driver, we point out that a secular tailwind exists for Monro in the form of electric vehicles, which are significantly heavier than traditional ICE vehicles. This added weight means that tires wear out on EVs at a faster rate than ICE vehicles, which will prompt a shorter replacement cycle. Of course, this tailwind is likely to take much longer to manifest for Monro given the fact that a majority of vehicles serviced are older ICE vehicles. There is also a risk to Monro’s service business as EVs begin to make appearances in the company’s service bays, but there are likely to be untapped service opportunities for the company in the EV space as well such as brake and brake fluid servicing.

Valuation

As you might expect based on analyst expectations and the multi-year selloff that the stock has endured, Monro is plumbing its historical valuation depths.

On a forward basis, the stock is currently well below its 10-year averages of 27.9x forward earnings and 13.1x EV/EBITDA expectations.

We also point out that, historically speaking, the stock has not typically remained at these levels for long, with valuations rebounding back towards the norm when valuations have reached these levels.

Our discounted cash flow (DCF) model suggests an upside as well once margins and operations normalize for the company. As a note, we are always cautious about DCF modelings since they are incredibly sensitive to subjective inputs and therefore difficult to validate (garbage in, garbage out, etc). For our model we have assumed a resumption of normal margins (EBITDA at 13% per our estimates and EBIT at 6.3%). We have also assumed a tax rate of 30% and that capital expenditures will remain sub 3% of the company’s gross revenues.

We further estimate a weighted average cost of capital (WACC) at 7.5% and an exit EBITDA multiple of 11x to arrive at an estimated fair value of roughly $50 per share.

Internal Changes

In addition to the dividend paid by the company, Monro is not shy about using capital to repurchase its own shares, buying back roughly 7% of the outstanding float in 2022 (current share count stands at roughly 31.4 million).

While investors are always happy to hear about share repurchases, Monro has also engaged in something distinctly less sexy, but in our view much more important. In its press release for the FY 2023 earnings, Monro announced a plan to declassify its board.

For those unfamiliar with board structure and operations, this is an unusual move. An unclassified board is a board where all members are generally up for election at the same time, while a classified board only puts up a slate of a few directors at once for re-election. As you might expect, a classified board makes a company much more difficult for activist investors and shareholders to enact meaningful change, while a declassified board makes it easier (maybe feasible is the right word here?) for large investors or groups of investors to make changes at the board level for a company.

According to the new plan, all of Monro’s directors will now serve 12-month terms and be up for re-election each year.

You can probably guess that this is odd—after all, it seems to be against the director’s personal interests. It is also odd for a board to declassify, generally (this is the first such time we have seen a board de-classify without significant activist or shareholder pressure).

At any rate, we think the change is unequivocally good: it raises the bar of accountability for directors and makes the company suddenly more interesting for large potential investors who may develop an interest in the company.

Some Risks

Of course, no investment is ever ‘safe’—every potential for reward comes with risks. While we think that the inherent commoditization of Monro’s business is a risk, as well as its reliance on macro conditions (household balance sheets, cost of materials, etc), we also think the company has an internal risk in its use of supply chain financing.

Over the last 18 months or so, the company’s days payables outstanding has jumped dramatically. Here is the note from Monro’s most recent 10Q regarding its payable financing (page 13).

In other words, instead of owing its suppliers, Monro will pay banks or other institutions who purchase the receivables from Monro’s suppliers. While supplier terms can vary from industry to industry, it is unusual to see supplier terms of 360 days. This has the effect of, essentially, delaying Monro’s bills.

While this can be a great way to conserve capital in the near term, it can also pose a risk, for obvious reasons. We think this figure is important to watch going forward to see how Monro leadership handles the payments or to see if the amount of outstanding payables reaches an unsustainable level.

Concluding Thoughts

The bottom line, for us, is that Monro operates a needs-based business: people can only delay replacing tires or otherwise servicing their cars for so long. Despite the headwinds the company has faced in the last two years (inflation, consumer wallet pressure, etc), we think that the current stocks current levels and valuations present a decent risk/reward ratio as inflation cools and margins and revenues return to normal levels.

Thank you for reading, and please consider subscribing to our newsletter!