Despite A New CEO, Starbucks Still Has A Long Way To Go

If you can't imitate Chipotle's success, steal their CEO.

Big Burrito, Big Day

January 26th, 2006 was a big day in the stock market. The hottest IPO of the year dropped, and investors couldn’t get enough. The stock price of said IPO increased by 100% on the first day. In the months following its debut, the stock’s P/E surged from 34x to nearly 80x—a testament to investor’s confidence.

So, what stock are we talking about here? No, it isn’t a high-flying, cash-incinerating tech company. We’re talking about: Chipotle CMG 0.00%↑.

In the relatively ho-hum corner of the market occupied by food and beverage companies, Chipotle has virtually always stood apart from its peers. With a tech-like multiple and tech-like revenue growth, investors everywhere are always on the hunt for the next Chipotle. Imitators, of course, came along, hoping for just a bit of that Chipotle magic to rub off on them and their stockholders (El Pollo Loco LOCO 0.00%↑ comes to mind).

The degree of enthusiasm for the chain seemed to mimic a similar national infatuation that spread throughout the U.S. in the 1990s and 2000s: the rise of Starbucks SBUX 0.00%↑. The coffee chain, with its distinctive green logo, was seemingly everywhere (in some cases, locations were right across the street from each other).

Over the years, however, the growth-stock shine has worn off of Starbucks. Founder Howard Schultz has left and returned to the CEO role a dizzying amount of times. The company has shifted focus from being a ‘third place,’ where people can spend hours talking, working, and drinking coffee, to being more of a grab-and-go establishment, with smaller stores being built to accommodate this strategic shift.

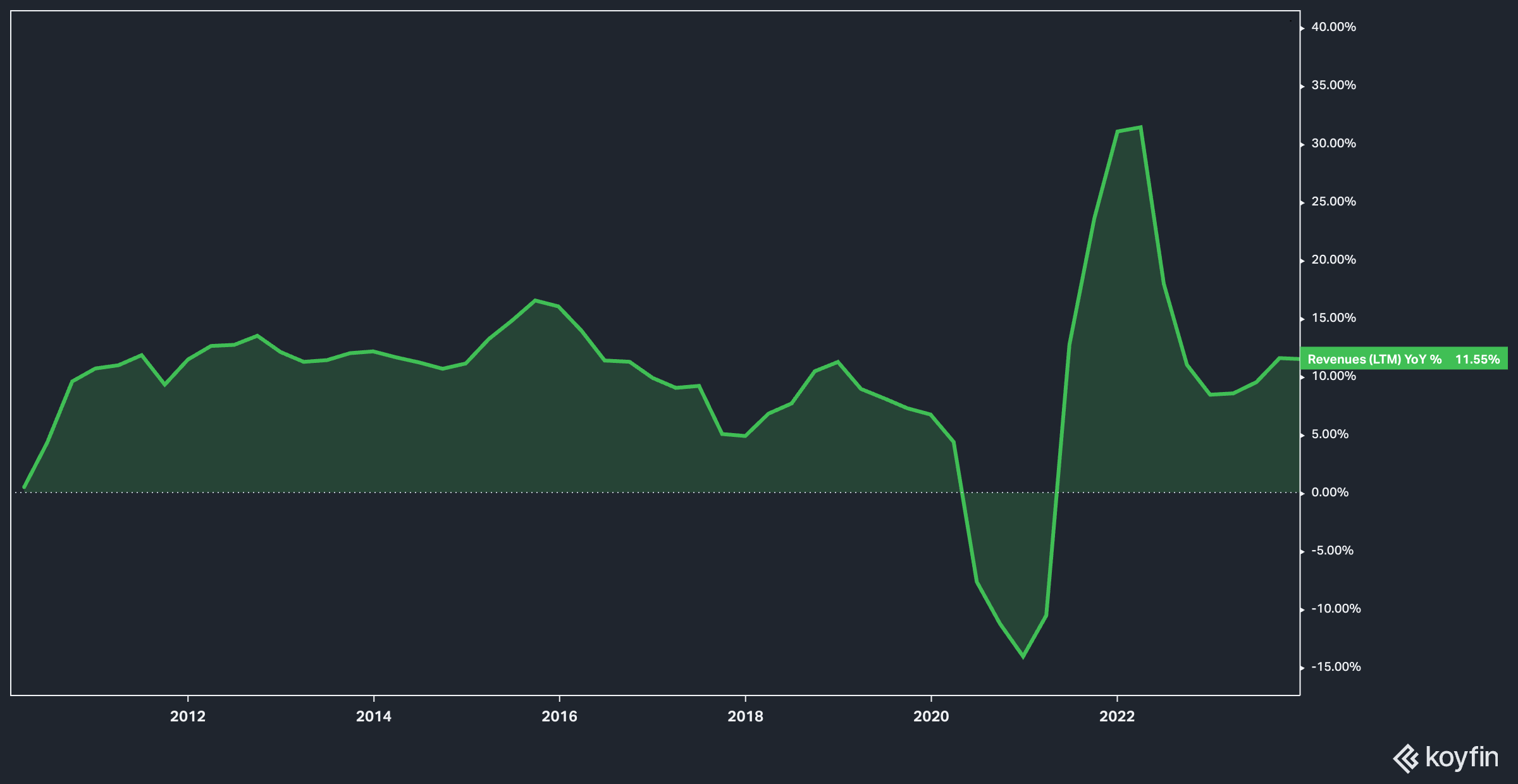

The market, meanwhile, hasn’t seemed excited about Starbuck’s prospects for some time. While the company handily beat the wider market SPY 0.00%↑ over the last 20 years, the last 10 years have seen some underperformance.

In response to slowing sales growth in the 2010s, Starbucks ventured east, making major investments in China (such as the launch of its Yunnan Farmer Support Center in 2012) to grow its business there and recapture some of the mojo that had faded from the American market. Executive Belinda Wong, who heads up Starbucks Chinese business, began to be featured prominently in Starbucks earnings calls as early as 2014.

The hiring of Laxman Narasimhan to the CEO role last year was, at first, a bit of a head-scratcher (he didn’t come from coffee), but made a lot more sense when you consider his former role as the head of the company which makes Lysol, a company for which China is so integral that he spent his first week as CEO of the disinfectant company in the country.

At any rate, this international expansion has proved very important for Starbucks, as domestic U.S. store count growth has stalled out. In the latest quarter, executives noted 4% growth in store count as the goal for the U.S. (as recently as 2021, U.S. store counts were contracting).

In a sense, though, Starbucks’s international expansion has done its job well enough. Top-line sales year-over-year increases have remained largely steady throughout the 2010s and into the 2020s (excusing the major drop and jump due to COVID).

In another sense, however, growth at Starbucks has become increasingly lackluster over the years, with international expansion making up the lion’s share of overall store growth.

According to data from Starbucks and Statista (visualized above) Starbucks’s store growth has essentially flattened, increasing by 10% in only one year out of the last 10.

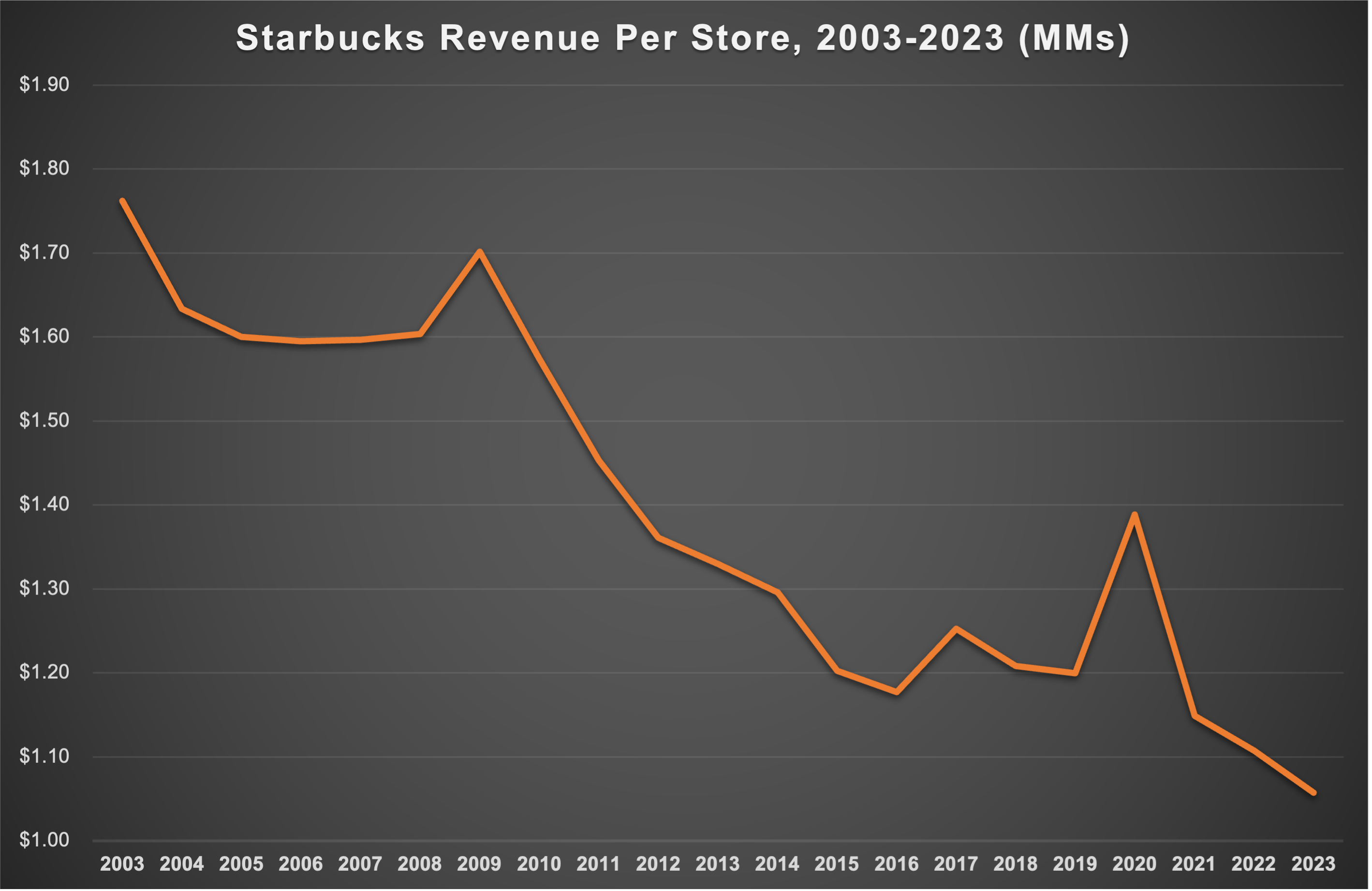

In the meantime, this store count has not correlated to an increase in sales per store.

In 2003, Starbucks averaged $1.76 million per store (sources: here and here). With a few years of exceptions, the downward trend has reigned supreme. 2021, 2022, and 2023 all saw declining per-store revenues of $1.15, $1.11, and $1.06 million, respectively.

It seems clear to me that the obsession with store count cannot continue as we can only conclude that each new store heaps overhead on the company while bringing in less revenue per location.

But again, this really is symptomatic of a larger issue: Starbucks seems to want to be seen as the growth company it once was, despite clear evidence that it no longer is, and must rely on increasingly fragile international markets to keep up the appearance.

When it comes to U.S. sales, it can easily be argued that Starbucks has hit a ceiling. And, I would argue—that’s not a bad thing. There are plenty of companies that have matured out of their early growth stages and succeeded as mature companies while maintaining market share. Take Apple AAPL 0.00%↑ and Costco COST 0.00%↑, for example). Both of these companies experienced years of explosive growth that, today, would be impossible to replicate even if they tried. And yet, these stocks and companies are beloved by shareholders and consumers alike.

In my humble opinion, Starbucks should take an honest look in the mirror and accept that yes, its hair is going gray.

But… that’s not the avenue they’re taking.

Starbucks Thinks The Grass Is Greener

(This section Is going to be light on numbers and heavy on reasoning, so I apologize in advance. But I think it gets to the heart of Starbucks’s core problem in a more meaningful way than analyzing earnings projections.)

The dismissal of Narahimhan as CEO only after one year and the hiring of Brian Niccol away from Chipotle is… weird, for a lot of reasons but makes a bit more sense when you consider my above reasoning that Starbucks wants very much to be defined as a company that grows.

I think that, at some level, this move reflects a fundamental disconnect between the board and where things at the company currently stand. This is not a groundbreaking idea—Starbucks employees have long felt that the company moves at odds with what they perceive the be the true spirit of the company.

While I don’t sit on the Starbucks board and can’t pretend to know what is discussed behind closed doors, the public-facing actions of Starbucks’s leadership points to a concern that there is something the company can do domestically to re-ignite growth. Narasimhan was a hire that onboarded international expertise which Niccols, quite simply, does not possess. Therefore, while my thesis about Starbucks’s self-diagnosis may not be the only conclusion one can draw, I have to think it’s at least a logical conclusion.

So. Does Starbucks have a domestic U.S. growth problem that can be fixed in a meaningful way? Or is this decline in domestic growth secular, something happening no matter what Starbucks wants?

While I concede that those are massive questions, I think they are ones we can grapple with. After all, this is business, theoretical physics.

It’s eminently unclear what exactly Starbucks could do to re-ignite growth, and this is not a trivial point. Very often companies in the midst of a turnaround or that are failing have leadership that is disconnected from public perception of the brand. For example, at Apple pre-Jobs’s second return, the consensus was that their products, for lack of a better word, sucked.

In other words—sometimes what’s wrong with a company is obvious. In Starbucks’s case, it’s not.

Sure, Niccols might scrap low-margin or low-selling items from its menu (indeed, this is already happening as the company announced it was ditching the Princi brand of baked goods). These sorts of reductions will could lead to an improved bottom line, but it won’t propel the company forward in the way I think the board of directors wants.

Starbucks has already moved to revamp its stores to prioritize drive-through and quick service over being a place where you can sit and read or work for long stretches (the famous ‘Third Place’ championed by Howard Schultz), and this has failed to re-ignite growth.

So… what would do it? We’ve already established that sales per store has been on the decline. The company has already tried to streamline stores, stretching barista capacity to the limit. Starbucks is arguably at near-peak saturation when it comes to the U.S. market.

Indeed, it seems to me that Starbucks will need an Apple-like reinvention in order to re-ignite strong growth in the U.S. What kind of idea is that? Frankly, I don’t know. And, unless Niccols is a QSR visionary in the mold of Steve Jobs, my guess is that there will be multiple proposals that ultimately fail to deliver in the U.S. market.

Analysts, for their part, seem to believe the stock is fairly priced, with the stock currently traded right at the average analyst price target. Maybe more importantly, the stock seems to be tagging along with EBIT estimates, which have been pretty stagnant for the last five years (barring the COVID recovery, obviously). For new readers, I far prefer EBIT to EBITDA for these comparisons as EBITDA is… not a useful metric since it can be inflated through accounting shenanigans.

All of this—expectations, store count, etc—also must be considered against the backdrop of rapidly rising COGS for Starbucks, with coffee futures hitting 10-year highs and concerns about the sustainability of coffee production rising.

Wrapping It All Up

Starbucks is an interesting case because it is somewhat difficult to quantify exactly why I’m bearish on the stock, except pointing to the fact that I believe Starbucks is now a mature company desperately trying to get its growth mojo back. The company is largely the victim of:

Its own success, and

secular forces beyond its control outlined above.

For these reasons, I’m taking a neutral-to-negative stance on Starbucks’s stock, as I do not believe it will be able to achieve the growth that its leaders think it can.

Disclaimer: The content in this article is for informational, educational, and entertainment purposes only. This content is not investment advice, and individuals should conduct their own due diligence before investing. The author is not suggesting any investment recommendations—buy, sell, or otherwise. This article is not an investment research report but a reflection of the author’s opinion and own investment decisions based on the author’s best judgement at the time of writing and are subject to change without notice. The author does not provide personal or individualized investment advice or information tailored to the needs of any particular reader. Readers are responsible for their own investment decisions and should consult with their financial advisor before making any investment decisions. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned. Any projections, market outlooks, or estimates herein are forward-looking statements based upon certain assumptions that should not be construed as indicative of actual events that will occur. Any analysis presented is based on incomplete information, and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. The author expressly disclaims all liability for errors and omissions in the service and for the use or interpretation by others of information contained herein.