Headwinds At Carter's

Exploring whether the children's retail chain presents a compelling opportunity a today's levels.

In this week’s equity deep-dive, we take a look at Carter’s, Inc CRI 0.00%↑, the largest children’s clothing retailer in the U.S. As always, nothing here is investment advice, please see the disclaimer at the bottom of the article. Cheers!

Tough Times

It’s been a rough few years for retail stocks. The whipsaw of the pandemic, supply-chain snarling, and building inventory at major brick-and-mortar retailers have left many investors scratching their heads at what to do with the sector. Those with slightly longer memories, however, are likely to recall the fact that the sector has been a bit of a laggard for some time.

On a ten year basis, the SPDR Consumer Staples ETF XLP 0.00%↑ has trailed the broader market by 92% on a price return basis. The past three years have been slightly better, but not by much: during that time frame the sector has returned 1.87% vs SPY 0.00%↑’s 25.8% return, as of this writing.

And yet, the sector has been known to hold some gems: consider the fabled run of Destination XL DXLG 0.00%↑, the men’s plus size clothing retailer that boomed from $0.26 per share in January 2021 to a peak of more than $8 in November of that year.

Today, we’ll dive in to see whether children’s retailing giant Carter’s has the potential to deliver as well, or whether more pain is likely to be in store.

Price & Valuation

Before getting too far in the weeds, let’s do a quick overview of where the stock has been and its current valuation.

Things haven’t exactly been rosy for the last five years. In that time frame, Carter’s has returned negative 21.8% on a total return basis for shareholders.

Given this decline, it’s not surprising that forward valuations have contracted.

With a current forward EV/EBITDA of 8.2x and P/E of 11.1x, the stock is trading below its five year averages of 9.6x and 13.8x, respectively.

While it may be tempting to view lowered forward valuations favorably, there are several macro conditions affecting Carter’s business which signal that perhaps the company is cheap per se, but that the market may be fundamentally re-rating it.

Demographics

It doesn’t take a rocket scientist to deduce that, for Carter’s, more babies = more business. The narrative of a falling birth rate in the United States has generally been a point of contention for investors looking into Carter’s—after all, while presumably people will continue to have babies at some level, perhaps the total addressable market for Carter’s will be much smaller than it was previously.

Carter’s executives seem to take some issue that it’s all bad news out there, however.

Speaking at the Goldman Sachs Global Retailing Conference in September 2023, Carter’s CEO Michael Casey had this to say in his opening remarks:

Birth rates have been stable, thankfully, after a nearly 14-year decline in birth in the United States following the Great Recession in 2008. Birth stabilized in 2021. There were forecasted to be 0.5 million fewer children born in 2021 following the pandemic. The experts were wrong. Births actually stabilized. There's an interesting change in human behavior following the pandemic. Births stabilized. It actually remained consistent in 2022. So we're encouraged by what we're seeing in birth trends, 60% of what we do for a living is baby apparel. It's a high-margin business and it's a less discretionary purchase. So we're encouraged by what we're seeing in birth trends.

The data appears to back this up in the near term, although the long-term trend is pretty abysmal:

While not a dramatic uptick, the birth rate per 1,000 people rose from 10.9 in 2020 to 11 in 2021. According to Macrotrends, the data has even improved since then, with an estimated 12 births per 1,000 people in 2023.

Further adding to the tentative optimism about future customers, 2022 was a banner year for weddings, which have been on the decline in the U.S. for decades. Last year an estimated 2.5 million weddings took place, the most since 1984.

Looking a little further back in the consumer ‘pipeline,’ Signet SIG 0.00%↑ CEO Ginny Drosos has been quite vocal about the expectation of cyclical growth in the engagement ring sale portion of her business (Signet is the largest jeweler in the U.S., owning the brands Zales and Jared, among others).

According Signet management, COVID created a dating lull. Given that their data show that the average engagement occurs 2.35 years after the relationship begins, they are expecting that business will pick back up to pre-pandemic levels shortly.

[W]e had predicted that we would see a lull in engagements caused several years ago by COVID now. So typically, pre-COVID, 2.8 million engagements per year in the U.S., last year, 2.5 million, this year, 2023 will trough at 2.1 million to 2.2 million, but then that begins to come back starting in our fourth quarter, and we believe creates a 3-year tailwind on our business, if we just maintained our market share, which is around 30%, that's $600 million in revenue that we see as part of those midterm goals.

In other words, it appears that the doom-and-gloom of the doomsday demographers may not come to pass in its entirety. Having kids typically follows marriage (or so I was told in an old rhyme), and so it seems that major concern about the long term strength of Carter’s business can be if not put to rest, then at least reduced from a five-alarm fire to something more manageable.

Even the popular narrative that younger generations (Gen Z and younger Millennials) don’t seem to match up with reality—according to a survey from the Thriving Center of Psychology, 83% of the younger generation aspire to be married someday, with only 1 in 6 of those surveyed stating that they don’t plan to get married (and, of course, as anyone who has been on this planet for more than a few trips around the sun can tell you, life tends to pan out differently than you expect).

Whether or not I’ve put to rest the ‘supply’ question for Carter’s is a matter of opinion, but it does seem that the evidence shows that the structural headwinds that have faced the business over the last few decades are at least slowing. This, of course, doesn’t change the fact that the long-term trend continues to be negative. Much more time will have to pass before anyone will be able to definitively say that demographics are suddenly working in Carter’s favor.

Demand

The big narrative around retail has been something akin to a snake passing a large animal through its body—after the initial supply chain shock of the pandemic, big box retailers loaded up on too much inventory and, over the last few quarters, have undergone ‘destocking,’ which is just a fancy term for: we’re putting stuff on sale and not bringing in new inventory because we bought too much.

The Great Destocking™ impacted big retailers differently, but Target TGT 0.00%↑, Walmart WMT 0.00%↑, and Amazon AMZN 0.00%↑ all felt some degree of inventory pain. These three are essentially Carter’s largest wholesale partners.

Addressing a direct question about destocking from Goldman Sachs analyst Brooke Roach, COO Brian Lynch had this to say:

I think the, I guess, "destocking", I feel like most of that is kind of behind us now. I think folks got in trouble last year of inventory when inflation hit hard and it started last summer that folks not only had too much patio furniture, but they felt they had too much apparel as well.

So there was some cancellations, there were destocking last year and then the supply chains weren't performing at a high level. So product were coming in later than folks who had requested it, and they had too much inventory to begin with. So that was kind of a situation that occurred out of Q2, Q3 and early Q4 last year.

However, from viewing the chart above, Walmart’s inventory build was significantly less than the build from Amazon (whose inventory levels, one can argue, is a much more difficult company to extrapolate meaningful data from), and that Target still remains above historic inventory levels.

So, while the worst of the Great Destocking may be past in the eyes of management, we certainly haven’t fallen back to pre-pandemic levels at some of Carter’s largest wholesale partners.

Performance & Outlook

Despite the optimistic tone from management that destocking is more or less a thing of the past, the stock market has clearly not agreed with the sentiment thus far. To evidence this, sales from 2019 to 2022 declined by roughly 13% while the stock declined by 27% in the same time period.

Judging by the data from Q2, it’s tough to blame the market.

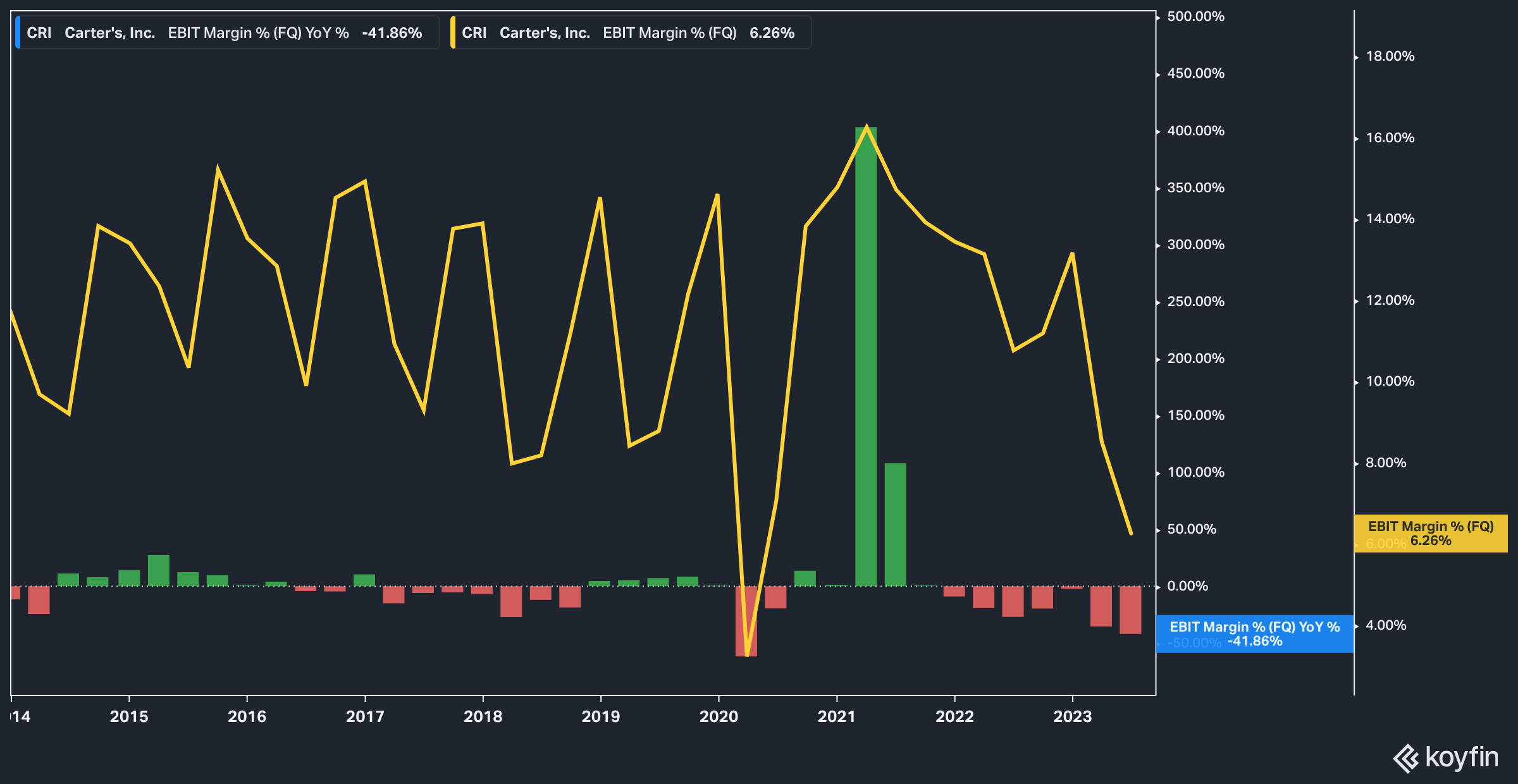

What I’d like to highlight here is operating margin, which fell by more than 40% year over year, and is part of a larger story of margin contraction for the company.

For the past seven quarters, year-over-year EBIT margin comps have contracted, while Q2’s EBIT margin print was the lowest in 10 years excluding the prints at the start of the pandemic.

Normally, falling margins to this degree would generate a bit of contrarianism—after all, margins generally revert. Whether pricing input pressure abates or companies capture more price from customers, margins generally find their way back to the average.

The only issue with this is the fact that EBIT margin isn’t the only symptom of underlying issues. From 2011 to 2019, Carter’s cash conversion cycle averaged 94.9 days. From the end of 2020 until the time of this writing, the average has been 99.2 days, with Q2 posting the highest level seen in 10 years at 160 days.

Inventory health is also showing signs of trouble—average inventory turns for Q2 were 1.9x, much lower than the ten-year average of 3.2x. Days inventory outstanding have also been climbing steadily over the last two years to well above historic norms.

The Bottom Line

Carter’s does not operate a bad business—children will always need clothing, and Carter’s offers fashionable choices for parents at affordable price points. It’s just unfortunate for the company that so many macro trends have been working against it for so many years.

Today, I view the company as a pass, but several things could change that, or signal a potential bottom and/or lead to a reversal of Carter’s fortunes:

Continued, sustained reversals in birth, engagement, and marriage rates.

A successful de-stocking of Carter’s own inventory.

An expansion of direct e-commerce sales.

Any continued period of deflation.

Further, as was mentioned above, a lower forward valuation alone doesn’t seem to be enough to stand on here: given the headwinds the company faces, it could just as plausibly be argued that the market has decided that a lower valuation is warranted rather than participants over-selling.

Disclaimer: The information contained herein is opinion and for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Factual errors may exist, and while they will be corrected if identified though the author is under no obligation to do so. The opinion of the author may change at any time and the author is under no obligation to disclose said change. Nothing in this article should be construed as personalized or tailored investment advice. Before buying or selling any stock, you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal, and readers should not utilize anything in our research as a sole decision point for transacting in any security for any reason.

Brilliantly written. Great analysis.

Thank you!