Idea Roundup #5: An Offer They Want To Refuse

In this week's Roundup: Uber, Snap, and more. Plus, Adam Neumann wants to buy WeWork.

Welcome to another week’s Idea Roundup! A quick reminder to please read the disclaimer below as everything that follows is my opinion and not investment advice. As always, please be sure to comment, share, and subscribe!

1. Uber Technologies (UBER) UBER 0.00%↑

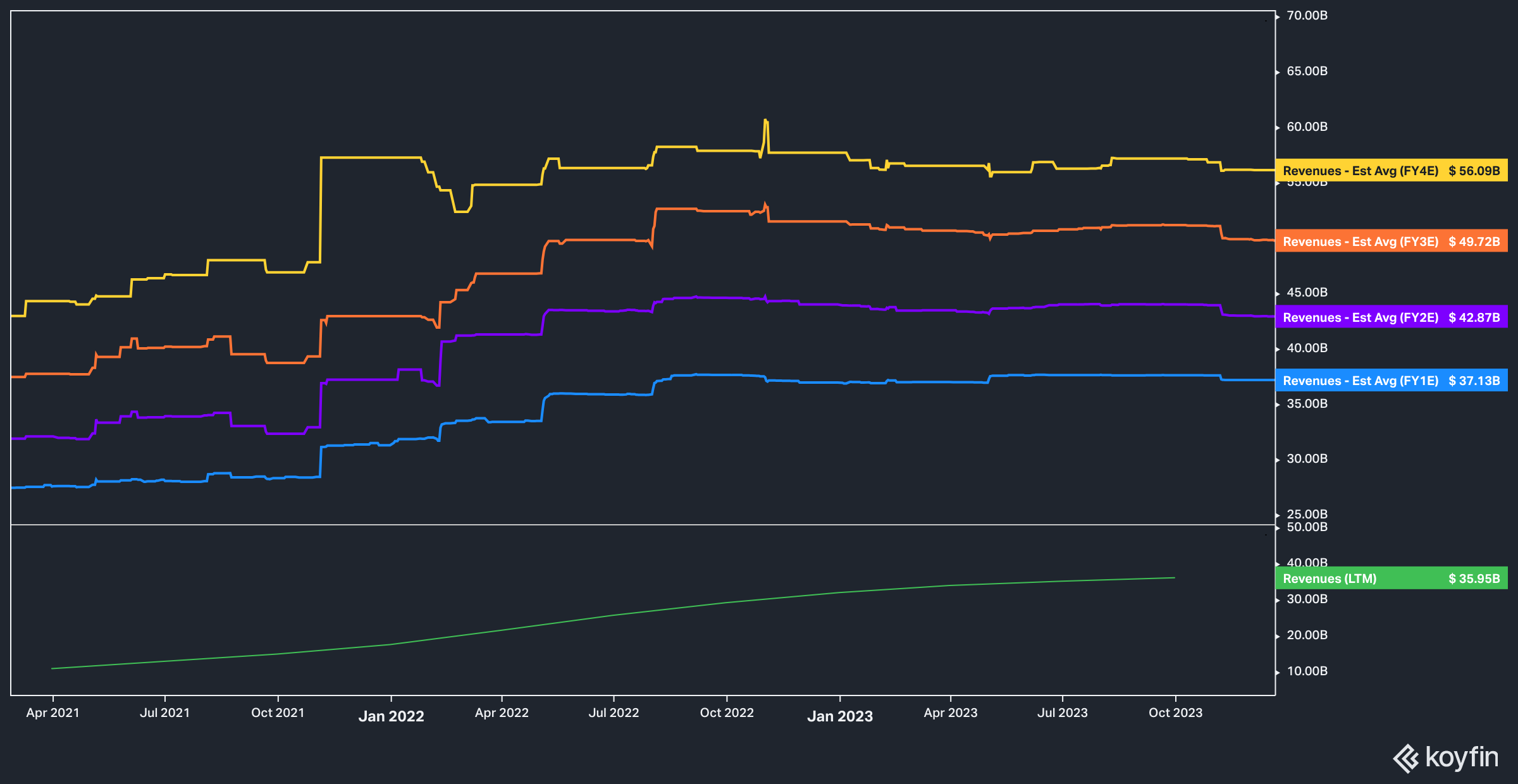

Uber dropped its fourth quarter and full-year results on February 7th to much applause. The ride-sharing-slash-food-delivery service capped off its full-year by delivering sales of $37.2 billion against estimates of $37.1 billion ($9.9 billion was delivered for the fourth quarter against $9.7 billion estimates). Most importantly, the company achieved a full-year net profit of $2.1 billion versus a $9 billion loss in 2022.

Management will surely take a victory lap on the earnings call, which will be happily cheered on by investors who have seen their shares surge by 107% in the last year. And, to be sure, they should.

The market, however, doesn’t tolerate excessive victory laps. Now that Uber is profitable, it won’t be long before investors are forced to ask the perennial question:

What’s next?

Uber has had an admirable turnaround under CEO Dara Khosrowshahi, but the newly profitable company still trades at a rich valuation—40x forward earnings and 27x EV/EBITDA. Before the dominance of the turnaround narrative, Uber was considered a growth stock. What is it now?

It would be difficult to call Uber a ‘growth stock’ today given that estimates for growth have essentially flatlined over the better part of a year. Far from being the sexy, younger version of itself posting mid-double digit growth rates and beating Lyftt LYFT 0.00%↑ to the punch on everything, Uber now has a dad-bod (and Lyft is, I don’t know, living in its mom’s basement or something). In other words, today Uber is just another company that makes some money and has a sky-high valuation. Sigh.

Of course, there’s nothing wrong with that, if (if!) that’s the sort of investment you’re looking for. In this author’s humble opinion, however, Uber’s stock is likely to have to reckon with this identity crisis soon.

2. Air Products & Chemicals (APD) APD 0.00%↑

The problem with steady-Eddie business that just kind of hums along without any major surprises is that… well, they don’t do a lot. Procter & Gamble PG 0.00%↑ and Coca-Cola KO 0.00%↑ aren’t exactly topping the lists of the most recent Barron’s roundtable despite having world-class operations. Even further down the staid, boring list of plodding companies sits Air Products and Chemicals, an industrial gas manufacturer and supplier.

In what may prove to be a trademark Mr. Market Overreaction, APD disappointed on its February 5th earnings, missing revenue and EBIT estimates by ~$200 million and ~$74 million respectively, sending the stock down 15.5% for the day.

The result? APD now trades in the nether regions of its historic forward P/E estimates.

Even more interesting, however, is the fact that ADP’s share price has meaningfully dissociated from its forward GAAP EPS projections:

I find this a bit surprising given the aforementioned clockwork of ADP’s business. As time marches on, of course, investors will continue to wonder whether the deal ADP brokered with Saudi Arabia to provide hydrogen to the fever-dream utopia city of Neom will bear fruit, and perhaps disappointment on this front is icing on the cake for tired investors.

3. Snap, Inc. (SNAP) SNAP 0.00%↑

Ah, where to begin? The social media company-slash-camera company reported disappointing earnings on Wednesday, sending shares into a 35% nosedive. After an impressive 2023 that saw the stock rip upwards 89% (though most of that gain came from November-December of the year), this earnings miss clearly stings.

But is there value in the drop-off? Well, when it comes to Snap, it’s tough to say. On the fundamental side, there’s not a lot to love:

The founders still wield an iron grip on governance via the company’s dual share structure.

Snap has not yet achieved the degree of scale of, say, Facebook META 0.00%↑ or TikTok, and at this stage in the company’s life it’s unclear whether it will.

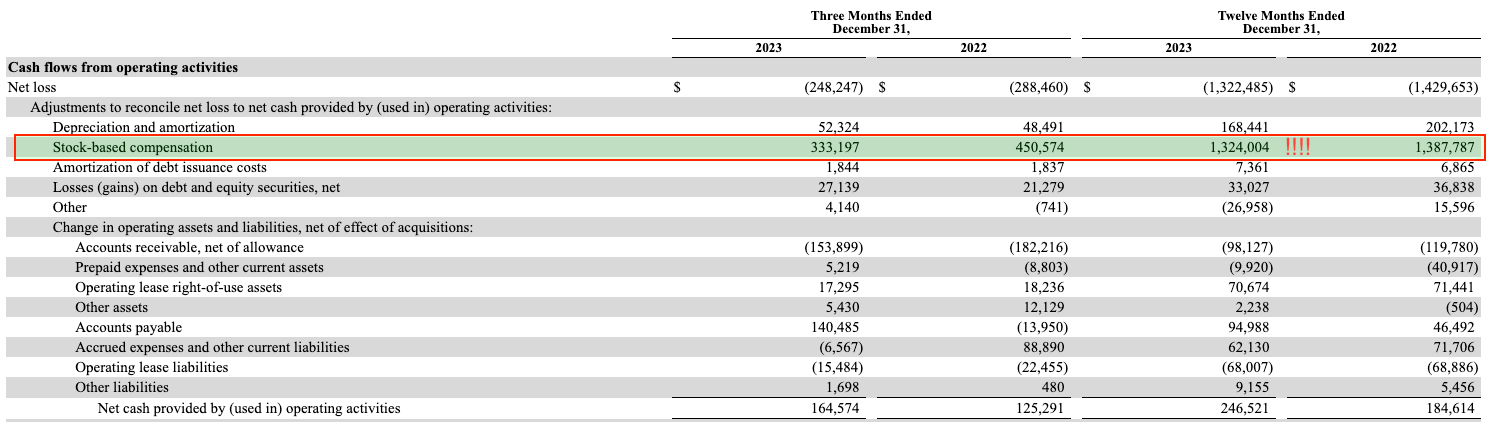

Top-line revenues essentially flatlined year over year with $4.6 billion in 2022 and… $4.6 billion in 2023.

Management hands out stock like candy—$1.3 billion worth of candy in 2023 to be exact.

Not even layoffs and hype around machine learning could get investors excited. Per the FT:

Coming a day after announcing sweeping lay-offs, Snap said in an earnings report on Tuesday its revenues increased 5 per cent to $1.36bn in the fourth quarter, below expectations of a rise to $1.38bn. This reflected “a challenging operating environment”, it said in a letter to investors.

In its letter, Snap said it had made progress on wielding machine learning to boost its advertising performance for brands, and that it had succeeded in increasing the number of small and medium-sized advertisers in particular.

While management seems to be making money hand over fist with Snap stock, it’s tough to see how investors will.

If you haven’t already, be sure to check out my latest equity deep dive on MasterCraft!

MasterCraft: A Beaten Down Stock With a 22% FCF/EV yield

Cyclical companies are, by and large, a tough breed for investors to tame. The opacity of cycles and the accompanying mania or depression of the collective investor crowd make it difficult for investors to think objectively. With that in mind, I think a great saying to lean on when evaluating stocks—and cyclical stocks, in particular...

4. Palantir (PLTR) PLTR 0.00%↑

Speaking of hype, it’s time to talk about Palantir. The data analytics firm reported sales for 2023 to the tune of $2.2 billion against 2022’s sales of $1.9 billion. The company also touted in its press release that this earnings release constituted “Its Fifth Consecutive Quarter of GAAP Profitability”.

The market, as is it prone to do, accepted this and sent the stock flying upwards 30%. Digging into the numbers, however, seems to show the same old cracks in the foundation.

While Days Sales Outstanding (DSO) fell to 60, they remain elevated above the company’s average of 49 days.

Palantir posted $119 million in income from operations (it posted an operating loss of $162 million in 2022). Interestingly enough, accounts receivable grew by $106 million (41% year over year compared to 16% revenue growth).

Were it not for the pile of interest-earning cash, Palantir may well have posted a loss as it incurred ~$15 million in interest and other expenses.

The Market Beat - Thoughts on Financial Goings On

An Offer They Want To Refuse

Everyone knows the old line about an arsonist offering to sell fire insurance, but what if the arsonist made an offer to buy the smoldering dwelling?

Apropos of nothing, Adam Neumann is reportedly trying to buy WeWork out of bankruptcy. Per Dealbook at the New York Times:

WeWork filed for bankruptcy this past November. In a restructuring plan filed with the bankruptcy court on Sunday, the company said that it had more than $4 billion in secured debt alone and that major creditors included SoftBank. At a court hearing on Monday, lawyers for landlords and others complained that WeWork may not have enough money to pay rent.

Some experts have suggested that WeWork could be sold for a fraction of its outstanding debt, perhaps for as little as $500 million.

Also:

Neumann’s new real estate company Flow Global is pushing WeWork to consider its takeover approach, according to a letter his lawyers sent to WeWork’s advisers on Monday. Flow which has already raised $350 million from the venture capital firm Andreessen Horowitz, disclosed in the letter that Loeb’s Third Point would help finance a transaction. (Read the letter.)

Flow has sought to buy WeWork or its assets, as well as provide bankruptcy financing to keep it afloat.

But Flow’s lawyers accused WeWork of stonewalling for months. “We write to express our dismay with WeWork’s lack of engagement even to provide information to my clients in what is intended to be a value-maximizing transaction for all stakeholders,” wrote the lawyers led by Alex Spiro of Quinn Emanuel, who also represents Elon Musk and Jay-Z.

While Neumann’s lawyers may be dismayed over the fact that management isn’t exactly salivating at the opportunity to bring back their old boss under whose leadership instituted “community adjusted EBITDA”, the rest of us are probably not.

I guess the real question I have here is—why does Neumann want this at all? The man walked away from WeWork with a half-billion pay package and has already roped Andreessen Horowitz into his new and strange real estate venture, Flow. Why go back?

The answer may be as simple as ego and pride, of course, but it doesn’t seem to make even basic business sense. On page 91 of the latest 8K filed by the company, the balance sheet reads as follows:

At first glance it may not look like a company in need of bankruptcy protection—there’s $1.1 billion in equity, after all! Despite the losses on the income statement, perhaps there’s something worth buying here. Upon further inspection, however…

WeWork lists its right-of-use lease assets at $2.6 billion, while its long-term lease liabilities sit at ~$4.5 billion.

There is a $2 billion asset line for intercompany loans. In a nutshell that’s money that a company lends… to itself.

An Investment in Subsidiaries worth $2.4 billion. There appear to be under the consolidation method, and it’s anyone’s guess whether or not the investment is still worth $2.4 billion.

In other words, while the liability side of the balance sheet is more or less solid (with the exception of Liabilities Subject to Compromise), the non-current asset portion seems… kind of squishy. Oh, and the income statement is a mess, too.

Of course, there are lots of people who specialize in exactly this kind of distressed investing—where I see trash another (more prescient and much smarter) investor sees treasure. But is Adam Neumann that kind of investor? Howard Marks is, sure, but Adam Neumann?

While I can’t definitively answer that question, I think I have a pretty good idea of it. Anyway, if this is, as I suspect, one big vanity project brought to us courtesy of Guys With Too Much Money, it’s quite a perplexing one.

Who knows—maybe commercial real estate will suddenly turn around and WeWork will achieve the scale and success of… Regus.

Disclaimer: The content in this article is for informational, educational, and entertainment purposes only. This content is not investment advice and individuals should conduct their own due diligence before investing. The author is not suggesting any investment recommendations—buy, sell, or otherwise. This article is not an investment research report but a reflection of the author’s opinion and own investment decisions based on the author’s best judgement at the time of writing and are subject to change without notice. The author does not provide personal or individualized investment advice or information tailored to the needs of any particular reader. Readers are responsible for their own investment decisions and should consult with their financial advisor before making any investment decisions. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned. Any projections, market outlooks, or estimates herein are forward looking statements based upon certain assumptions that should not be construed as indicative of actual events that will occur. Any analysis presented is based on incomplete information, and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. The author expressly disclaims all liability for errors and omissions in the service and for the use or interpretation by others of information contained herein.