Idea Roundup #9: Stop Trying To Make 'Bing It' A Thing

Plus: Gold to the moon? And are things really that bad at PayPal?

Thanks for reading the Idea Roundup, published weekly. As always, nothing here is investment advice. Be sure to read the disclaimer at the end—this is a work of opinion, not investment advice! Cheers—IR.

1. Zoom Video Communications (ZM) ZM 0.00%↑

Zoom is one of those rare companies whose name has achieved verb status. People don’t say, “I’m jumping on a video call,” they say, “I’m jumping on a Zoom,” sometimes even when they aren’t using Zoom’s platform. This rarified air is occupied by few other companies, such as Google GOOG 0.00%↑ GOOGL 0.00%↑, and envied by many others (stop trying to make ‘Bing it’ a thing, Microsoft MSFT 0.00%↑, it’s never going to be a thing).

Anyway, the last few years have painted a stock chart for Zoom that resembles Mount Everest, leaving investors who thought the boom times of the early COVID-19 days would never end in a tough spot.

While acknowledging that I write a decidedly subjective newsletter in decidedly subjective business, I can say objectively that this chart is ugly. Following Zoom’s peak, there were certainly plenty of bagholders left in the dust. But sometimes following this period of bagholding, value can be found.

For starters, Zoom is not like a lot of other tech companies out there, because it actually makes money. Like, real cash. The company also offers more than just video calling services—indeed, most of the company’s products involve a full suite platform of services resembling Microsoft Teams. This business has always taken a backseat to the company’s video chat feature, but management expects that the change soon.

The company is also dirt cheap, trading at just 12x forward earnings and 6x EV/EBITDA.

Also, the company’s board approved a $1.5 billion buyback of stock—which is nice and will help to offset the massive stock-based compensations expense that is the custom among tech companies.

The Quick Take: Bullish.

2. SPDR Gold Trust (GLD) GLD 0.00%↑

This marks the first time I’ve highlighted an ETF in an Idea Roundup, and why not? Gold, after all, is on a tear. Everyone’s talking about it. And we all know that when everyone is talking about a particular asset or trade or what have you, that said asset or trade can only continue to go up… right?

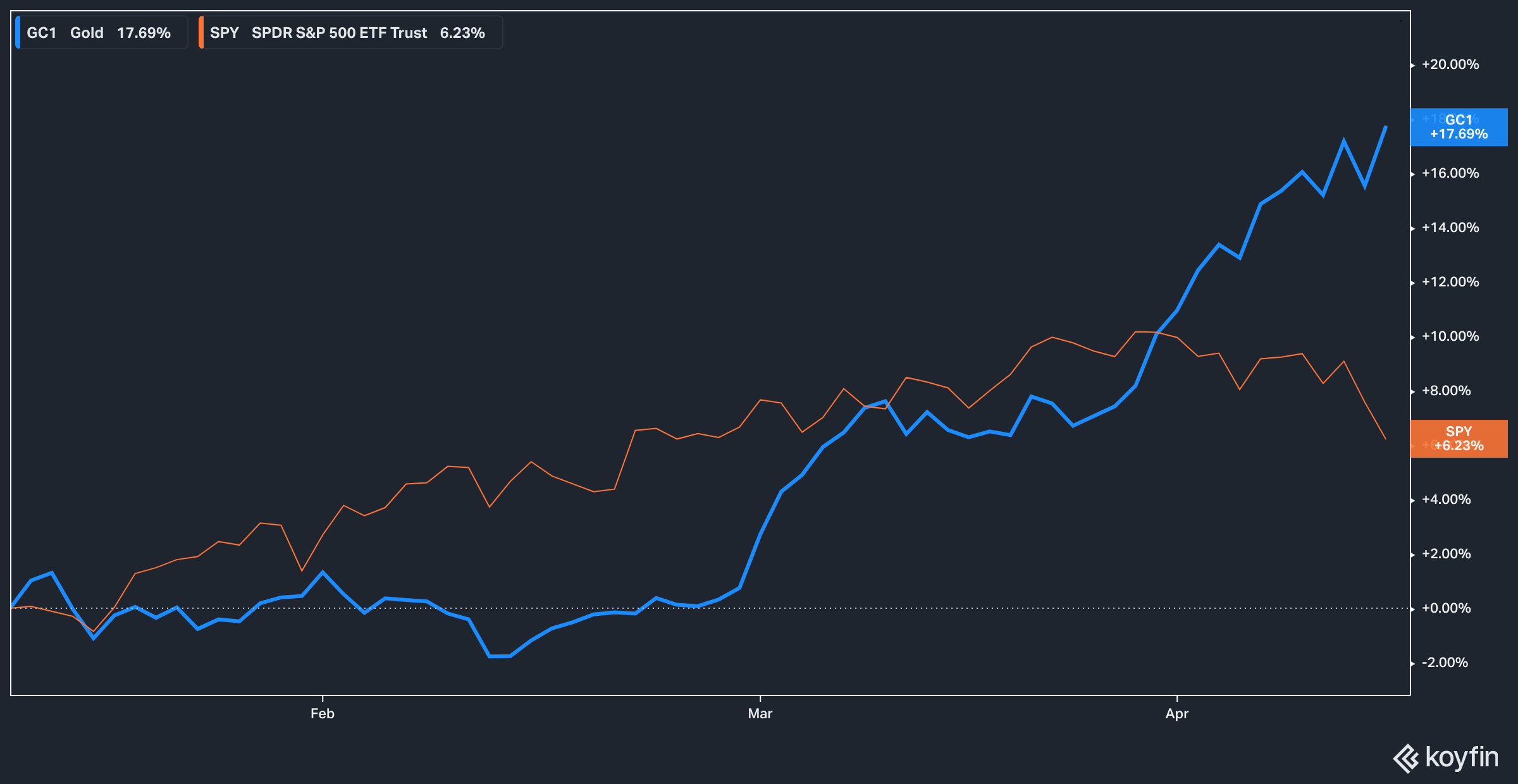

In the last three months gold futures have surged past the S&P 500 SPY 0.00%↑ by 11%, breaking out of the $2,000 range in February and sitting today near $2,400.

This surge is, on the one hand, a bit perplexing. Gold famously doesn’t pay interest or dividends, while bonds do. The fact that expectations for Fed rate cuts keep getting diminished should be (should be!) bad news for the yellow metal, but so far it hasn’t been.

On the other hand, it’s not very perplexing at all. Geopolitical tensions play a major role in the performance of gold, of course, and the general malaise of under-investment in the mining sector globally is certainly placing a strain on supply.

Demand, meanwhile, shows no signs of waning. With trust in government institutions at all-time lows around the world, it’s not surprising that people want a bit more gold in their portfolios.

At the end of the day, it’s difficult (impossible?) to make any pronouncement about where gold may be headed—after all, we’re one missile away from it surging through the roof, and one booming jobs or GDP report away from a plunge.

The Quick Take: Short-term neutral, long-term slightly bullish.

3. The Hershey Company (HSY) HSY 0.00%↑

Hershey has had a bit of a falling out with the investing public over the last 18 months or so. Allegations of higher-than-allowed levels of heavy metals in their chocolate, competition from a Gen-Z upstart brand powered by a major YouTuber, and negative reports from outlets such as

over at The Bear Cave have all served to depress this stock since around mid-2023.

Even though this company’s presence in its industry is more or less ubiquitous, and the fact that the furor over the Death By Ozempic trend has largely fizzled out, investors remain glum about Hershey’s outlook. In its latest earnings, the company missed its most recent top-line sales estimates by $65 million and whiffed on GAAP EPS by $0.19, coming in below even the most pessimistic analyst estimates.

Growth prospects also appear tepid, with only 2.8% top-line growth expected for FY2024 and a nearly 1% decline in net income for the same period.

For a deeper dive into this troubled giant, check out this piece from

:

My Quick Take: Bearish.

4. PayPal (PYPL) PYPL 0.00%↑

If you were to rank stocks that people currently love to have, PayPal would probably be somewhere near the top. Bears contend that the company’s products are undifferentiated, that ongoing consolidation in the payments industry makes competition more difficult, and that the exit of Elliot Investment Management portends badly for the company.

However, the pessimism may be overdone. PayPal has over 400 million active users and generates substantial free cash flow.

In fact, as the stock has been treading water at these current lows, a lot of metrics that investors generally want to see moving up and to the right are… well, moving up and to the right. Cash from operations, revenues, and free cash flow per share are all turning up. Meanwhile, shares outstanding have fallen by 10% since January 2022 as the company aggressively buys back its own stock.

Add to the mix the fact that you have a new management team in place that has already shaken up the senior leadership ranks of the company, and it’s not difficult to view PayPal’s situation with a little more optimism than before.

The Quick Take: Bullish.

Disclaimer: The content in this article is for informational, educational, and entertainment purposes only. This content is not investment advice and individuals should conduct their own due diligence before investing. The author is not suggesting any investment recommendations—buy, sell, or otherwise. This article is not an investment research report but a reflection of the author’s opinion and own investment decisions based on the author’s best judgement at the time of writing and are subject to change without notice. The author does not provide personal or individualized investment advice or information tailored to the needs of any particular reader. Readers are responsible for their own investment decisions and should consult with their financial advisor before making any investment decisions. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned. Any projections, market outlooks, or estimates herein are forward looking statements based upon certain assumptions that should not be construed as indicative of actual events that will occur. Any analysis presented is based on incomplete information, and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. The author expressly disclaims all liability for errors and omissions in the service and for the use or interpretation by others of information contained herein.