Market Brief: Recession Risk Is Back, Baby

Also: Homes are tough to come by, and the bond downgrades that never happened

Welcome to the Almost Daily Market Brief! Thanks for subscribing, and as always please feel free to forward or share this with anyone who may be interested. Cheers!

The Consumers Are Alright…?

It seems like the collective world of financial journalism has been predicting for the last decade that a recession is right around the corner. Covid? That’s a recession. Post-covid? That’s a recession. Rising rates? Oh, you better believe that’s a recession.

And yet, all of these things have not resulted (yet) in a recession, which has stymied experts up and down Wall Street. It’s yet another instance of the old saying manifesting itself: when everyone believes something will happen, it won’t.

So, with some cracks in the collective facade of Wall Street soothsayers appearing, should it be time to worry? Today, Bank of American CFO Alastair Borthwick (Man. What a name.) stated that “It’s difficult to see a US recession when the consumer is spending 4% more year-over-year.” Difficult indeed, Alastair.

While we can’t say we’re clearly or obviously moving toward a recession, the contrarian-indicator alarm bells in my head are ringing, especially when big wigs in the financial press begin giving the economic All Clear.

So, let’s take a look at some numbers to parse this out.

According to the Bureau of Economic Analysis, disposable personal income (pictured above) shrank in Q2 2023 for the first time in a year. Meanwhile, personal interest payments on a quarterly basis have ballooned from $313 billion in Q2 2022 to $479 billion in Q2 2023.

Of course, those interest payments are a function of interest rates, which are widely expected to level off at this point, and wages continue to grow, but the fact remains that the current resilience from the U.S. economy comes from one place (the consumer), and any contraction in disposable personal income (which is needed to fuel that resilience) should be noted.

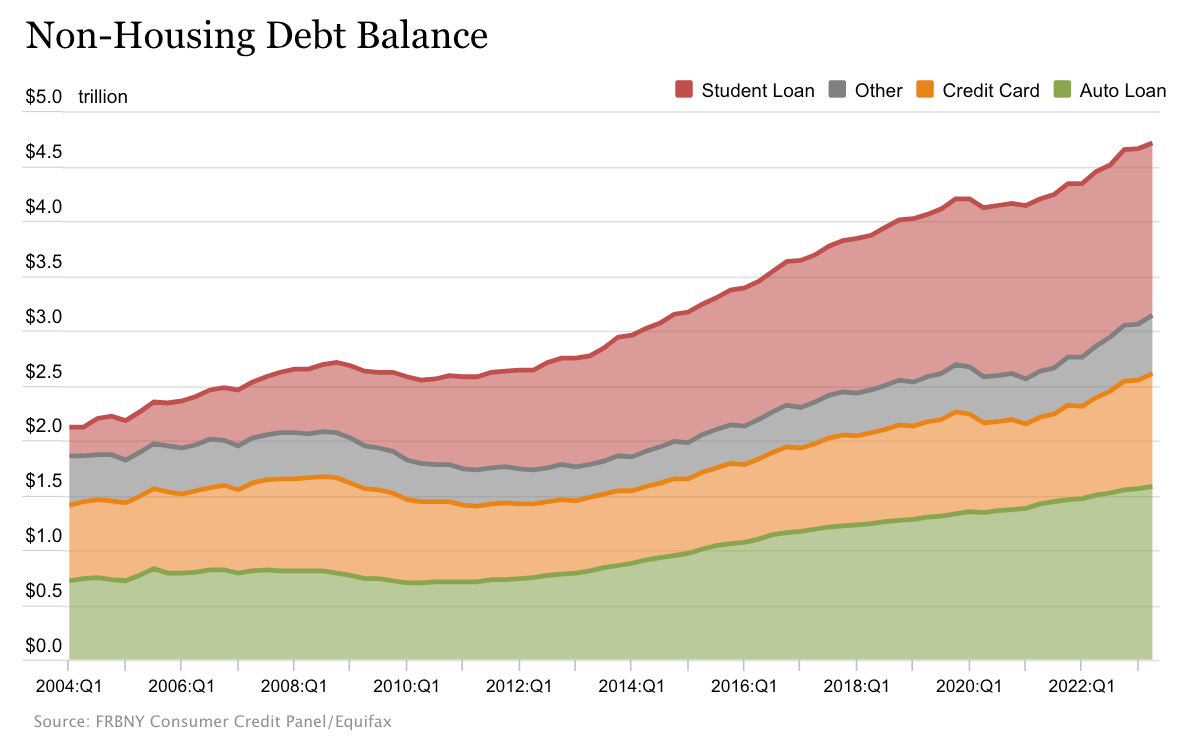

Pending resumption of student loan payments (in October) threatens this disposable income even further, as $1.5 trillion of the roughly $4.7 trillion of total personal non-housing debt is student loan debt. Credit card balances have also expanded at quite a clip, crossing the $1 trillion mark for the first time in Q3 2022.

Do I know that we’re going to be in a recession in the next year or so? No, of course not. Don’t be silly. I don’t know what I’m going to have for dinner tonight. However, the sentiment shift from Wall Street combined with a decline in personal net income and the pending resumption of student loan payments threatens to put a large swath of consumers in a bind.

Other News

Is almost-junk turning to junk?

An article appeared in Bloomberg this morning wondering whether or not the long-anticipated arrival of the credit bubble burst in BBB bond might have have been overblown. Overblown, because instead of seeing companies default in the wake of interest rate hikes, many corporate indentures have received upgrades from the rating agencies. In light what was discussed earlier in this note, I’ll leave you with this sentence from the article itself:

Of course, rating agencies have a reputation for being somewhat backward-looking (or outright wrong) and their categorization of any corporate bond can quickly change along with companies’ collective fortunes and the general economic outlook.

Even big guys can’t find homes to buy

It’s getting tough out there in the housing market. Housing starts—a measure of how confident builders are that there will be a buyer present when the final nail is hammered—fell to the lowest level since 2020. This does not portend well for general housing availability, which is already shockingly low given that a huge percentage of borrowers are sitting on low-rate mortgages and just don’t want to move. It’s gotten so bad that even massive single-home landlords are finding it difficult. As one executive told the Wall Street Journal, “We write hundreds of offers every week at price points that we’d be willing to transact at… We’re striking out quite a bit.”

Final Thoughts…

What to watch for Wednesday’s Fed meeting. China may be gaining ground against US chip sanctions with a new breakthrough. Sam Bankman-Fried’s parents are making headlines. Intel CFO warns that data center chip inventories may be too high. America’s problem isn’t too few workers—it’s their productivity.

Brilliant take!! Really enjoying reading your posts on substack

Thank you very much!