MasterCraft: A Beaten Down Stock With a 22% FCF/EV yield

MasterCraft: A Beaten Down Stock With a 22% FCF/EV yield

The pessimism on MasterCraft seems to reflect economic assumptions that are no longer likely to come to pass.

Cycles Come & Cycles Go

Cyclical companies are, by and large, a tough breed for investors to tame. The opacity of cycles and the accompanying mania or depression of the collective investor crowd make it difficult for investors to think objectively. With that in mind, I think a great saying to lean on when evaluating stocks—and cyclical stocks, in particular—is “You can have great news or great prices, but not both.”

With that said, today’s stock is MasterCraft Boat Holdings, Inc MCFT 0.00%↑, a small-cap maker of recreational boats. Its largest segment is Ski/Wake boats (sold under the MasterCraft brand) which range from $100k-$320k in price. The company also manufactures pontoon boats under the Crest brand ($35k-$220k) and luxury day boats under the Aviara brand ($200k-$1.3m).

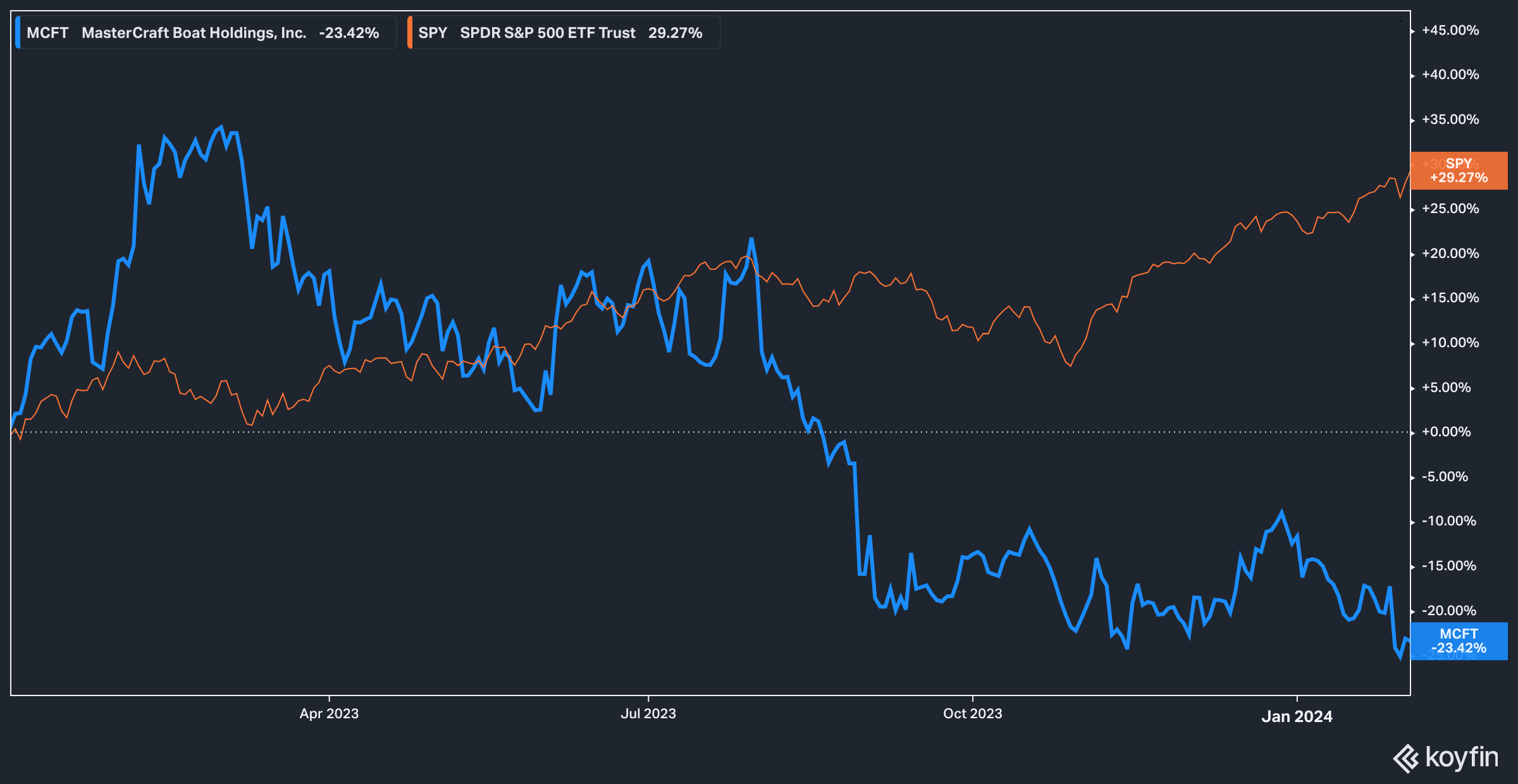

As you might imagine, COVID-19 provided a significant tailwind to the company as people sought to partake in different outdoor activities. The stock was boosted by a surge in sales during that time (after almost 80% in the flash recession of March 2020), but since the latest rally at the start of 2023, shares have since fallen more than 50% off their peak.

On a one-year price return basis, MasterCraft has underperformed the Russell 2000 by a significant margin. On a five-year basis the stock has also underperformed, delivering an 8% return against the Russell’s 38% price appreciation.

Despite this underperformance, I believe MasterCraft operates a top-notch business in its space with exceptional returns on capital. Further, the stock has felt the pain of both higher interest rates and the looming fear that recession is just around the corner—two headwinds that appear to be set to fade away in the coming year. Let’s dive in.

Note: If you’d like to get greater detail on the financial models used in my analysis, you can get them in my subscriber threads posted on Substack Notes. Subscriptions are free, so get access to this info by subscribing to Ironside Equity Research.

Current Problems

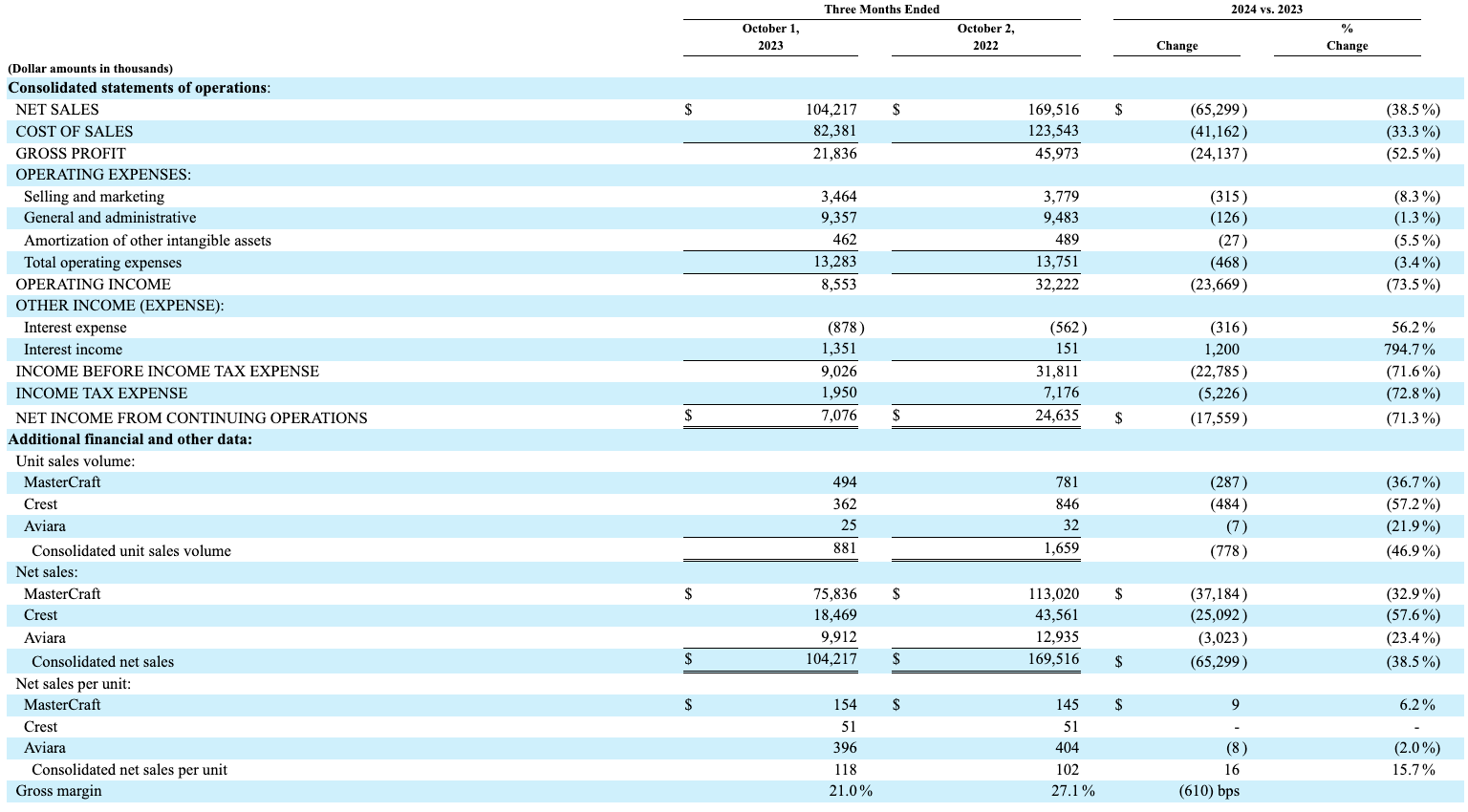

There’s a saying I love when it comes to investing, which is “you can have good prices or good news, but not both.” And today, the news at MasterCraft isn’t very good. The company’s previous quarterly results were more or less objectively horrendous.

Consolidated unit sales volume collapsed year-over-year by ~47%, led by a 57% drop in Crest (pontoon boat) sales, while Aviara (luxury day boats and the company’s smallest unit) took the smallest hit with a ~22% unit volume decline.

MasterCraft brand net sales dropped by $37 million, though the brand did benefit from a bit of price-taking. The culprit for all this? Management states in a note on page 18 of the latest 10Q that:

The net sales decrease reflects decreased unit volume and an increase in dealer incentives, partially offset by higher prices. Dealer incentives include higher floor plan financing costs as a result of increased dealer inventories and interest rates, and other incentives as the retail environment remains competitive.

These operational challenges are more easily met when you have a balance sheet like MasterCraft’s.

$174 million in current assets against $142 million in total liabilities gives the company some staying power during inevitable downturns. As further evidence of the strength of the balance sheet, MasterCraft has a net debt/EBITDA of just 0.2x.

Dealer Network

Dealer/floor-plan model businesses rely on the health and strength of the dealer network for the manufacturer to survive. Most of the boat industry is brand-agnostic, which means that dealers will sell any brand they sign an agreement with.

MasterCraft is a bit different in that regard. Per page three in the latest 10K:

The majority of our MasterCraft brand dealers are exclusive to our MasterCraft product lines within the ski/wake category, highlighting the commitment of our key dealers to the MasterCraft brand. Our other brands are generally served on a nonexclusive basis by their respective dealers.

The section goes on to state:

For fiscal 2023, the Company’s top ten dealers accounted for approximately 40% of our net sales and one of our dealers individually accounted for 14.9%, or approximately $98.6 million.

It’s understandable if this is a red flag for some—after all, a concentrated customer base means that the loss of one major customer can severely impact sales. In this industry, however, the likelihood of a great loss is, in my opinion, quite low. Unlike other ski/wake boat manufacturers, MasterCraft’s business model is more akin to a Chevrolet GM 0.00%↑ or Ford F 0.00%↑ in that dealers are captive.

Competitor Malibu Boats MBUU 0.00%↑ operates on a non-exclusive basis, and per their latest 10K, their top 10 dealers also account for ~40% of sales, essentially the same as MasterCraft.

The question, then, is if there is any meaningful advantage or disadvantage afforded MasterCraft by operating in this way. In boom times it probably doesn’t make a difference, or it would be slightly negative. Making dealers exclusive takes time and energy, whereas a non-exclusive dealer is a fairly easy sign-on.

In downtimes, however, the exclusive model becomes more of an asset, in my opinion. The ability to more closely monitor dealer floorspace and not be concerned about whether or not a dealer or network of dealers will suddenly allocate less floor space to your brand is, in many ways, a valuable asset.

Stacking MCFT Up Against Its Peers

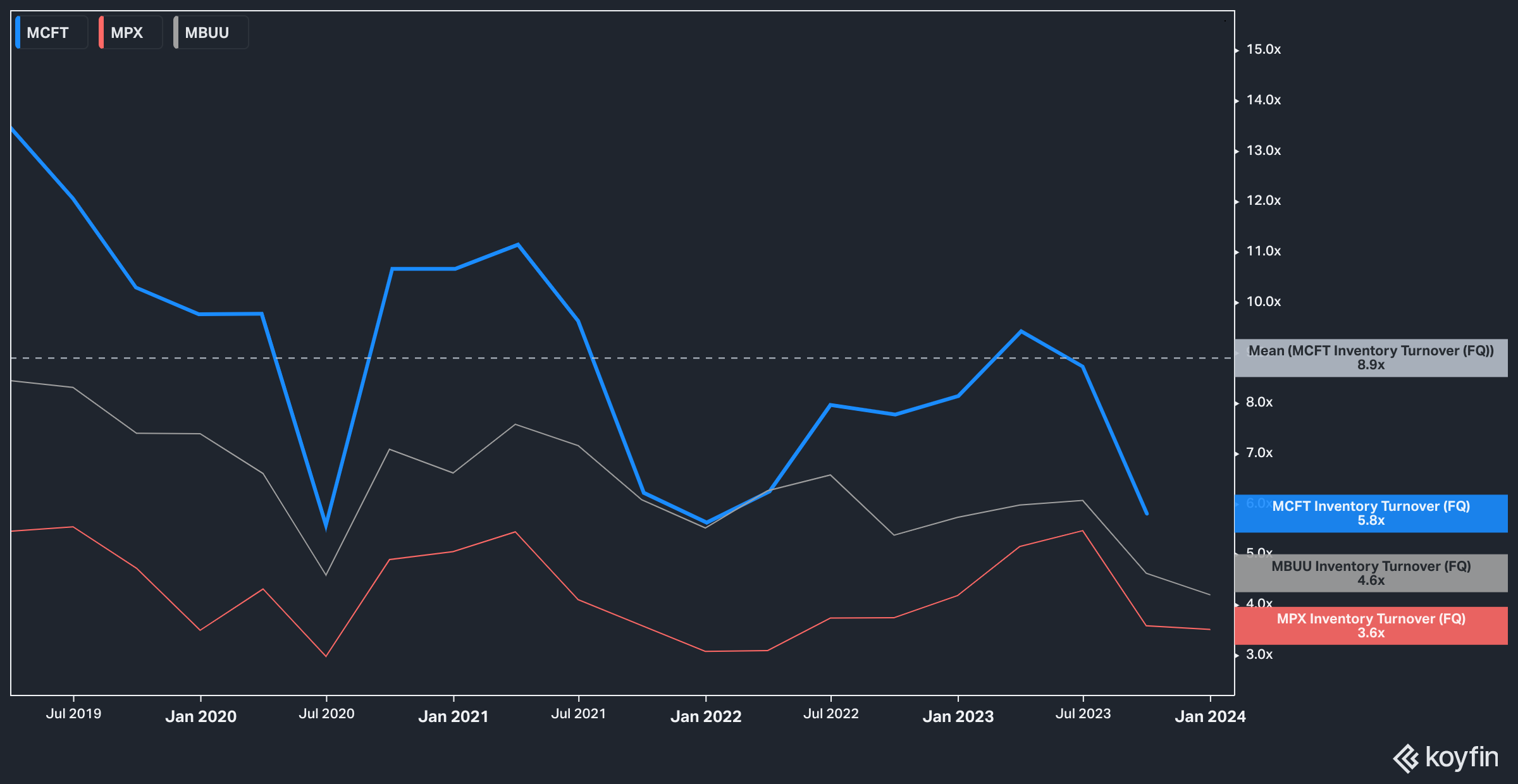

MasterCraft’s management team runs a tight ship, as evidenced by multiple performance metrics against peers Malibu Boats and Marine Products Corporation MPX 0.00%↑.

First up is inventory turns, a measure of how efficiently management can move inventory through the system and translate it to sales. Over the last 5 years, MasterCraft (in blue, above) has averaged 8.9x inventory turns per quarter, and despite the latest downturn the company turned inventory almost a full time more than Malibu and two times more than Marine Products.

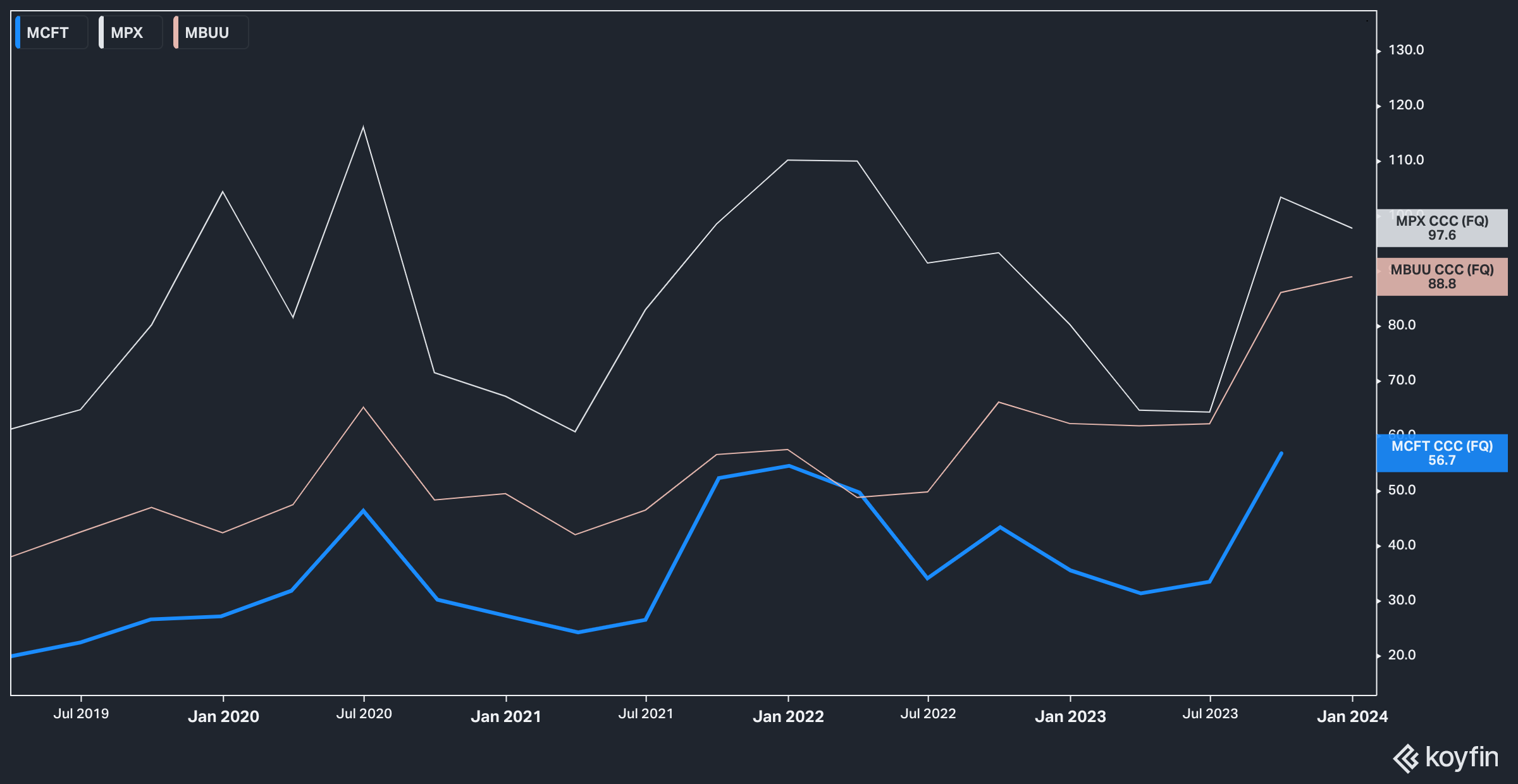

MasterCraft also is more efficient at getting actual cash through the door, as evidenced by a 56-day cash conversion cycle in the latest quarter against 88 days for Malibu, the next closest competitor. (While I can’t quite show it, I also suspect the better performance on this metric relates to the company’s captive dealer network.)

Despite this, the market has generally assigned a valuation premium to other competitors, such as Malibu.

With the brief exception of the early innings of the COVID-19 Pandemic and a stretch of 2023, over the last five years MasterCraft has trailed Malibu in forward earnings estimates.

On some level, this is perhaps not surprising given that Malibu posts sales roughly double MasterCraft’s but in this case size does not seem to lead to greater operational efficiency.

What’s Priced In

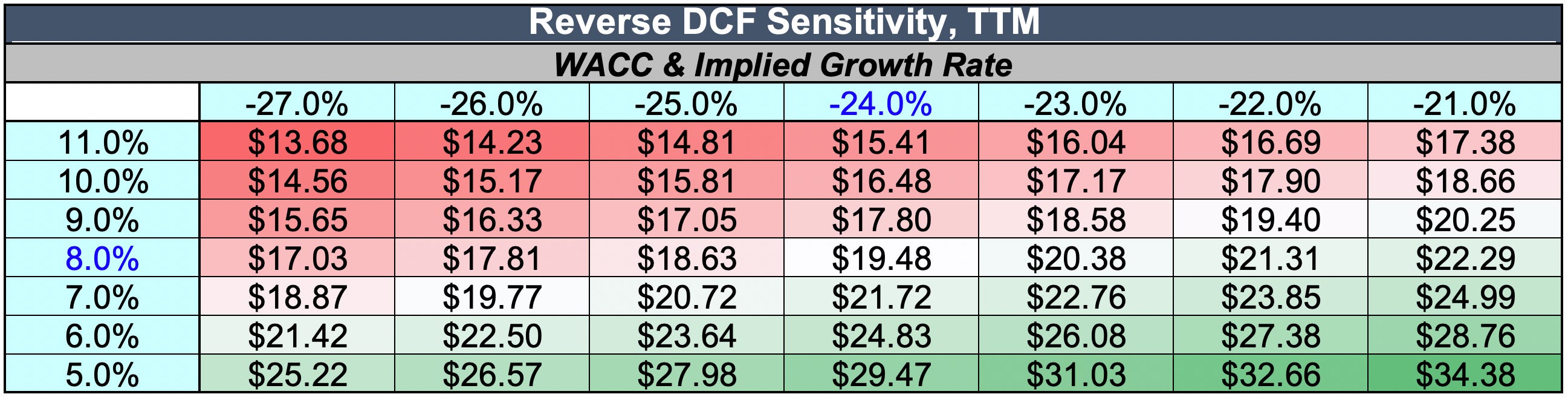

I say it a lot around here, but we humans aren’t exactly great at shrugging off recency bias. Financial markets aren’t much better—poor results today are typically expected to continue into the future, and that negative sentiment appears to be baked into MasterCraft’s current price according to my reverse DFC estimates.

Using an 8% WACC, it seems the market is baking in 5 years of 24% declines in annual sales—something that seems incredibly unlikely.

Note: A quick reminder that access to my reverse DCF and the associated assumptions will be posted in a thread for subscribers. Subscribe for free to Ironside Equity Research to get access.

Valuation

We’ve already briefly touched on MasterCraft’s low forward P/E (currently less than 11x), but other metrics paint a stellar picture of the company.

Against its own 10-year history, other consumer discretionary companies, and the wider U.S. stock market in general, MasterCraft ranks in the top decile for free cash flow / EV yield (an incredible 25%), buyback yield, and shareholders yield excluding debt.

Consider this again against competitor Malibu Boats, which has an FCF/EV yield of 6.9% and a shareholder yield excluding debt of 2.1%.

Drivers of Growth

Buying a ski, pontoon, or luxury day boat is a major purchase, and as such MasterCraft is subjected to the macroeconomic force of interest rates and inflation. As interest rates rose over the last two years, MasterCraft’s fortunes fell. Inflation also ate into consumer’s ability to find extra money for a boat payment each month.

The result was easy to see—the stock went down as investors feared that the Fed would keep rates higher for longer and that a recession was on the way. However, that recession seems increasingly unlikely to arrive, especially in an economy posting 3%+ growth year over year. The Fed also appears ready to cut rates in 2024, although those cuts may not come as soon as initially expected. Inflation has also moderated from its highs.

So, as inflation and rates begin to moderate, the expectation (which the market isn’t accounting for) is that MasterCraft’s outlook should improve.

Second is the growing popularity of pontoon boating as a recreational activity. Getting out on the water was something that people did in droves during the pandemic, and the MasterCraft’s Crest segment (a little less than 20% of total net sales) benefitted handsomely. The natural follow-on from this burst in activity was a sales hangover, with the brand’s sales dropping 57% year over year.

But pontoon boating appears to be more than a fad, and the pontoon boats of today bear little resemblance to the bulky, slow, cumbersome crafts of yesteryear (as evidenced by the fact that you can waterski behind many of today’s pontoon boats).

Research & Markets estimates that the total market for pontoon boats will grow to $3.9 billion in 2028, up from an estimated $2.5 billion in 2023. This growth means that MasterCraft’s emphasis on growing its pontoon business is well-placed.

Base, Bull, and Bear Thesis

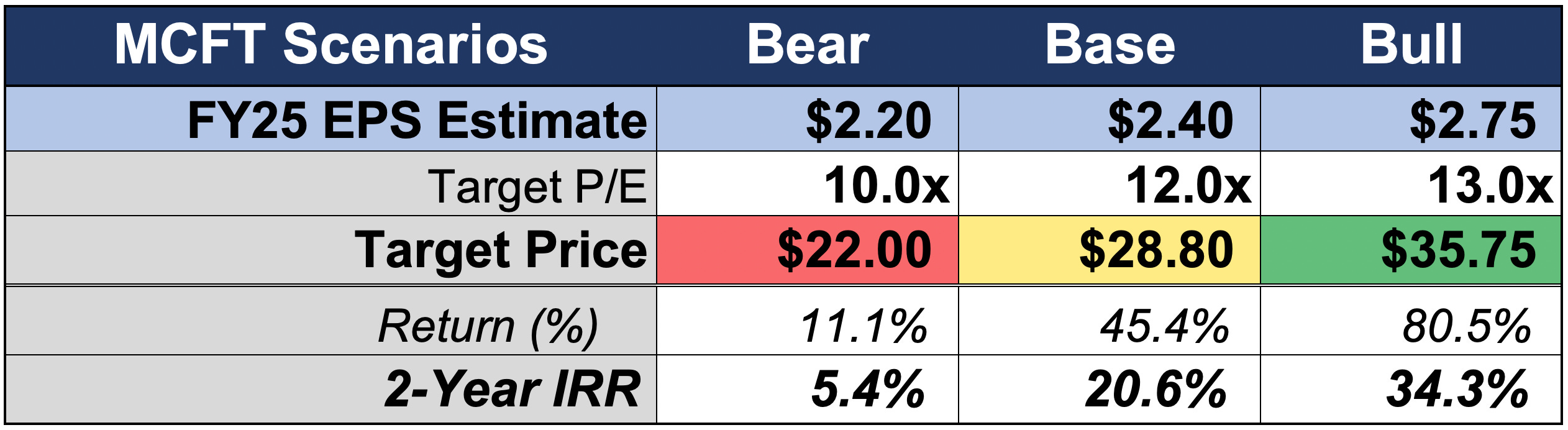

Analysts are quite negative on MasterCraft’s FY2024 outlook, with an average EPS estimate of just $1.70 per share, rebounding to $2.44 in FY2025. I set my base case EPS for FY2025 at $2.40, my bull case at $2.75, and my bear case at $2.20.

Let’s unpack this. There are a few reasons I think that MasterCraft is likely to revise its FY2024 guidance higher as we move through the year.

On the last earnings call (held November 8th, 2024), CEO Frederick Brightbill had this to say: “Macroeconomic factors, including interest rates, which could remain elevated for some time, are adversely impacting the demand for recreational boats and other luxury consumer goods. The potential for a broader economic downturn during fiscal 2024 could worsen this headwind for the industry.” Given that interest rates are expected to moderate this year and an economic downturn seems much less likely today than it was in November of 2023, I think this may be a tailwind for management guidance.

Dealers are currently sitting with a higher-than-optimal level of inventory, and the feeling of impending economic doom soured management on their ability to move that inventory. With, again, a better economic outlook, I think that the inventory may move faster than expected.

Management guided to $390-$420 million in net sales for FY2024 when forecasters were at their peak pessimism about the economy going into 2024.

Further, while 2023 was a disappointing year from a unit sales volume perspective, the blended average selling price per unit across all three categories climbed 33%, from $78k to $103k. This is probably unsustainable.

To arrive at an estimated $405 million in net sales for FY2024, I estimate that overall unit sales would have to collapse 26% to 4,701 (a level not seen since FY2018), and the blended ASP would have to fall 17% to $86k (still comfortably above FY2022s blended ASP).

One Final Reminder: If you’d like to see portions of my model that include the assumptions discussed here, I post them in the subscriber chat, so click the link below to subscribe if you’d like a bit more detail!

A better FY2024 than previously expected is not a crazy expectation, especially with expectations of a more robust economy. To repeat myself for the millionth time, this could be a tailwind in the near term. The outlook for FY2025, I believe, will also benefit from this, and the outlook, and while my current FY2025 base case reflects a reasonable earnings expectation, I think it could be revised higher should a better FY2024 come to pass.

Thank you for reading, and be sure to read the disclaimer below. Cheers, and happy investing!

Disclaimer: The content in this article is for informational, educational, and entertainment purposes only. This content is not investment advice and individuals should conduct their own due diligence before investing. The author is not suggesting any investment recommendations—buy, sell, or otherwise. This article is not an investment research report but a reflection of the author’s opinion and own investment decisions based on the author’s best judgment at the time of writing and is subject to change without notice. The author does not provide personal or individualized investment advice or information tailored to the needs of any particular reader. Readers are responsible for their own investment decisions and should consult with their financial advisor before making any investment decisions. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned. Any projections, market outlooks, or estimates herein are forward-looking statements based upon certain assumptions that should not be construed as indicative of actual events that will occur. Any analysis presented is based on incomplete information and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. The author expressly disclaims all liability for errors and omissions in the service and for the use or interpretation by others of information contained herein.

Nice write-up, enjoyed reading it. Thanks.

Thank you for the write-up. I come across Mastercraft like 2 times a year and are tempted each time.

How do you get to the FCF yield? If I look at the numbers, FCF LTM basis looks roughly like $50m, which gets you to c. 15% yield. Which is still not bad...