Staples Stocks Still Slumping

Plus: Stock picking may be down, but it's not out.

Consume This

We’ve talked a lot about the resilience of the American consumer around here, and how said resilience has perplexed economists and market-watchers. It’s odd, then, that one of the biggest market casualties of 2023 has been the consumer staples sector.

From the Wall Street Journal today:

The S&P 500 has declined 5.7% from its 2023 peak on July 31, while the SPDR S&P Retail exchange-traded fund, which includes the shares of 78 retailers from department stores and other apparel companies as well as automotive and drugstores, has dropped 13%. For the year, the broad market is hanging on to a 13% advance and the retail benchmark is off 3%, the widest spread since 2017.

Investors and analysts say higher gasoline prices, tighter credit conditions and sticky inflation are beginning to catch up with many consumers. U.S. consumer confidence has fallen for two consecutive months, underscoring Americans’ growing unease about their finances and the health of the economy.

“If food prices are high, if gas prices are high, I can buy less of the discretionary stuff that I want rather than need,” says Anna Rathbun, chief investment officer at CBIZ Investment Advisory Services.

All of that tracks. In fact, it’s kind of nothing new—we’ve been endlessly hearing about how households will be squeezed with each passing quarter, but without seeing the actual effects of the squeeze play through in the economy.

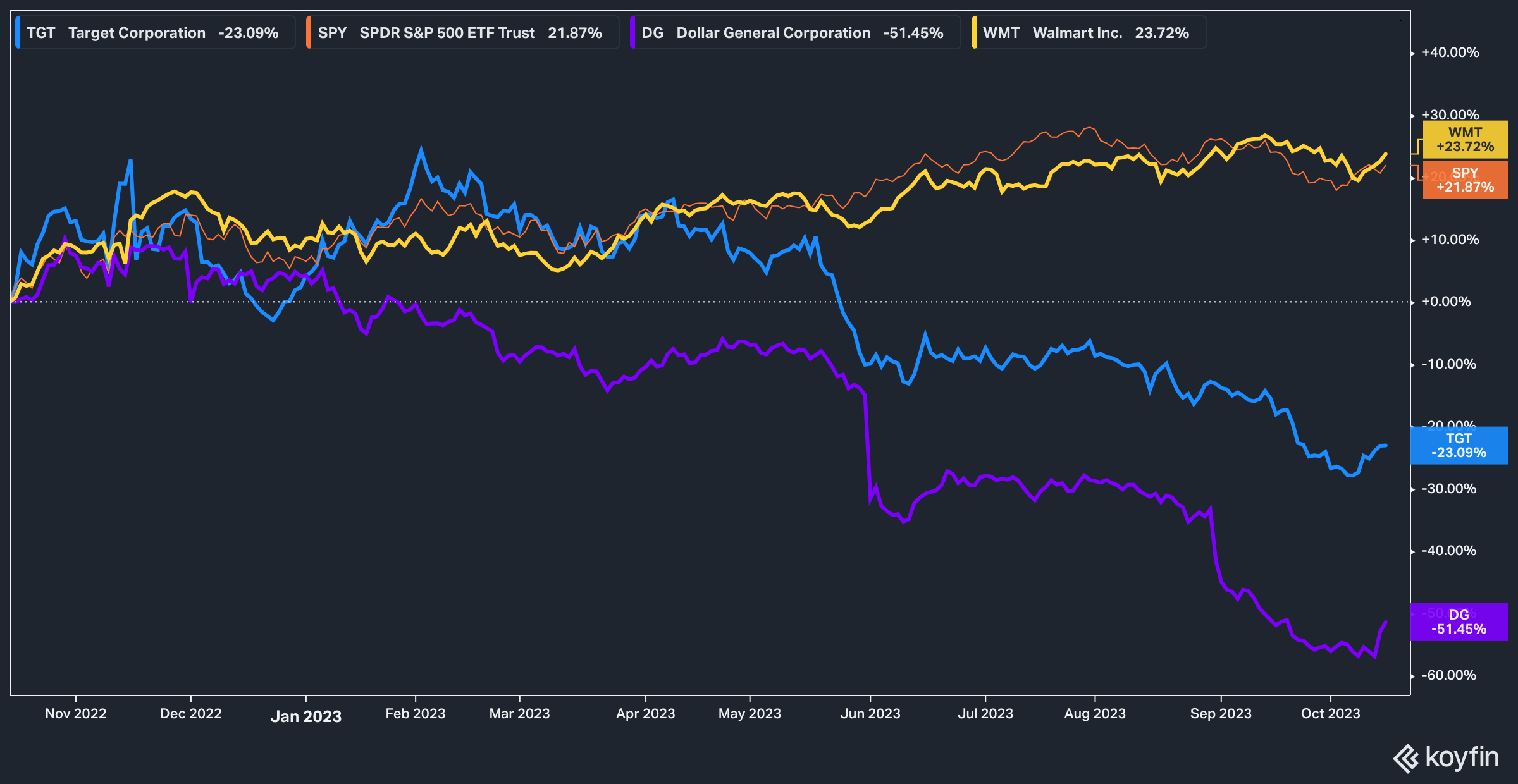

However, if you only looked through the lens of consumer staples stocks, you could be forgiven for believing that a full-blown recession was already upon us.

In the last 12 months, only juggernaut Walmart WMT 0.00%↑ has been able to generate a positive return for shareholders. Target TGT 0.00%↑ and Dollar General DG 0.00%↑ haven’t fared so well, with Dollar General carrying a large part of the retail sector’s woes on its shoulder as the poster child for weakening consumer demand.

All of this, in my humble opinion, is not likely to dramatically improve anytime soon for the sector in general, especially with the resumption of student loan payments this month (another fun topic we’ve touched on a bit here).

Don’t Count Stock Picking Out

Cheap money is the ultimate tide that raises all boats—when capital can be raised for virtually free, a few things happen:

Companies can make moonshot bets, or just generally take risks they maybe wouldn’t otherwise take.

Big institutions and investors that generally skew towards the risk-off side of the investing spectrum have to take more risk than they would otherwise take because, well, there’s no yield.

This makes for a weird market—it’s difficult for a company to fail. Unprofitable companies, for years and years and years, kicked the can down the road by rolling old debt into new debt at even lower rates than before in a weird cycle that, at the time, felt like it might never end.

The casualties of this market were the Masters of The Universe themselves: hedge fund managers with a buy-and-hold mindset, or a value tilt, or who simply couldn’t bring themselves to buy gobs of stock in unprofitable companies. The wider market simply left them behind.

Today, an article in the FT discussed this exact question:

But in the next year or so, the final bill will come due. A lot of companies are about to learn the hard way that they cannot roll over the money they borrowed at 2 per cent in 2020 at 2 per cent again in 2024. Try on 8 or 9 per cent for size, and good luck. Those paying back floating-rate debt are already feeling the pain of expensive debt servicing costs.Whether this builds up into a wave of corporate defaults or failures is a matter of intense debate in investment circles. Rating agency Moody’s said this week that speculative-grade (ie, riskier) companies in the US have almost $2tn of debt falling due between 2024 and 2028, up by some 27 per cent from its earlier study covering the four years to 2027. In the next five years, a record $1.26tn in safer corporate bonds also fall due.

Also this month, Goldman Sachs totted up the stats to show that, astonishingly, almost half of all US-listed companies in 2022 were unprofitable. “Higher funding costs could force some of these companies to cut labour costs or even close,” analysts at the bank wrote.

Not good! If you were to ask me how many publicly traded companies were unprofitable, the answer would have been “a lot”, but certainly not half.

Given the fact that the market is prone to overreact to good news while ignoring bad news until the sky is falling, it’s not surprising that the recent weak market rally has had legs. I don’t think I’m going too far out on a limb when I say that any future correction in the wider market will not affect all stocks equally, and that at that time the beleaguered active management crowd may once again have their place in the sun.

Final Thoughts…

Nvidia may face further restrictions on its chip exports to China. Schwab’s depositor flight is showing signs of moderation. Home sales are still stuck in a rut. Goldman wants out of the consumer lending business. Sounds like it shouldn’t be possible, but there’s a drought in the Amazon rainforest. Crypto-bros rejoice: crypto ETFs may be a thing soon.