WeWork Ain't Paying

Thoughts on the decline of the office-sharing company, PLUS: Chinese property developers and earnings season is upon us!

Welcome to today’s Market Beat! As always, please consider subscribing and sharing this with anyone who may enjoy it. Cheers!

WeDon’tPay

Office-space sharing company WeWork filed a notice last week that it would be withholding interest payments in the form of both cash and PIK notes on five of the company’s debt issuances. While presumably nobody needs a deep dive on the history of the troubled company (if so, check out this book or, for an even more abridged story, this miniseries), the cliff notes version of it goes like this: Adam Neumann started WeWork, pitching office sharing as an incredible, new idea (it’s not), and ended up getting billions and billions of dollars from the human cash bazooka named Masayoshi Son, the CEO of Softbank.

After a long, protracted, and bizarre struggle with the company, Neumann was eventually forced out with only $445 million to show for all his work. Not long after, the company went public and, well, things didn’t go so hot.

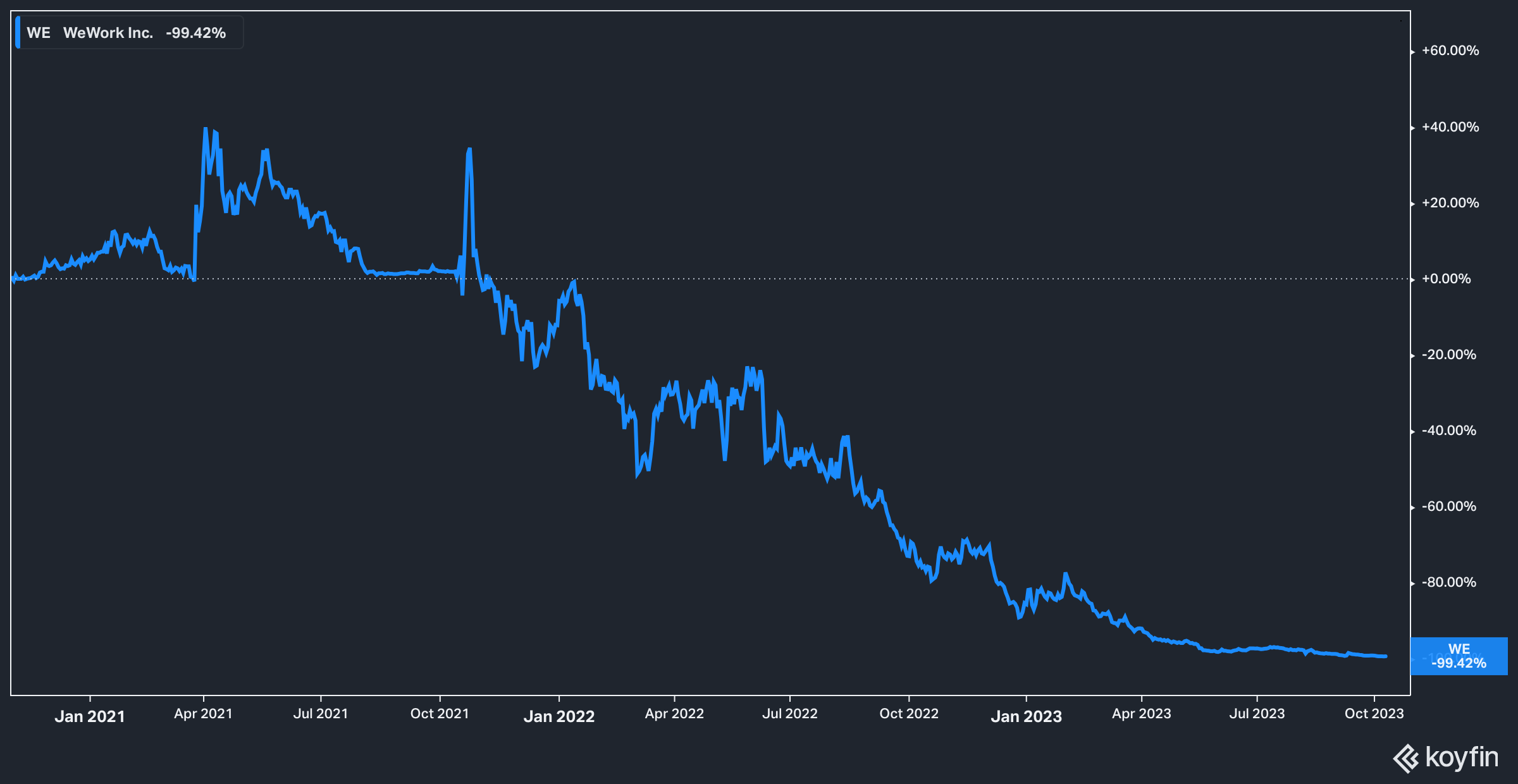

Since going public the stock has fallen by 99%, and today this one-time unicorn worth an estimated $47 billion in the private market has a market capitalization of $165 million.

In other words, the severance the company paid to Neumann today is roughly three times larger than the public value of the entire company.

Folks, that’s what we in the biz call value destruction.

Alright, back to the suspended interest payments. Here’s what the company released:

WeWork Inc. (the “Company” or “WeWork”) has elected to withhold aggregate interest payments of approximately $37.3 million payable in cash and $57.9 million payable in the form of additional PIK notes (together, the “Interest Payments”), each payable on October 2, 2023, with respect to WeWork Companies LLC and WW Co-Obligor Inc.’s following notes (collectively, the “Notes”)

The fact that the bulk of the company’s payments are composed of Payment In Kind notes is particularly jarring and shows the reality of the company’s situation.

Of course, a quick glance at the company’s balance sheet from the latest quarter shows that this was probably not hard to see coming. With only $205 million in cash on hand and a negative total equity to the tune of $3.5 billion, things are… not good.

The company plans to take the next few weeks to enter into restructuring talks with stakeholders:

Entering the grace period is intended to allow discussions with certain stakeholders in the Company’s capital structure to commence, while also enhancing liquidity as the Company continues to take action to implement its strategic plan. As part of this strategic plan, the Company is focused on rationalizing its real estate footprint and improving its capital structure.

Yeah, definitely seems like the right thing to do here.

In the sad story of WeWork, there are only a few losers and even fewer winners. Masayoshi Son of course lost billions, while Adam Neumann made out like the proverbial bandit. I wouldn’t even feel too bad for the current bondholders—the folks in that crowd are going to have a pretty good understanding of what they were getting into.

The other set of losers out there are, generally speaking, retail investors. With institutional ownership at roughly 13%, a whooole lot of moms-and-pops out there are likely to have watched their capital vanish as the stock price plummeted from $90+ per share to the $2.27 it currently trades at today.

While it’s easy to look at WeWork in hindsight and wonder about the hubris of the founder and the investors, it’s nonetheless entertaining to know that even people with billions of dollars can be taken by charisma. It’s not likely that WeWork will recapture anything close to its former glory, but the vultures of the financial world are likely to enjoy a pretty good meal off of it.

Earnings Season Is Upon Us

It’s the most wonderful time of the quarter—earnings season! With war breaking out, oil on the rise, and interest rates high, it’s certain to be an interesting one. Something that has befuddled investors for the last two years is just how companies have staved off reporting dismal results in the face of higher debt costs. The answer is, largely, that most companies took advantage of ultra-low rates and debt maturities are still relatively far off on the horizon. The day, however is coming, and for the most debt-ridden companies, it’s alreadyhere. Bloomberg notes:

Some $820 billion of US and European non-financial corporate bonds are maturing in the next 12 months. That’s about 7% of this market, according to data compiled by Bloomberg. While companies overall are not expected to run up against a maturity wall before 2025 onwards, debt-ridden companies are already feeling the pain from higher rates.

Further:

Goldman Sachs Group Inc. strategists led by David Kostin recently warned that borrowing costs for S&P 500 companies have already ticked up by the largest amount in nearly two decades, on a year-on-year basis. Of the 69 basis points of contraction in ROE in the first half of the year, nearly half came from higher interest expenses, they said.

Since the global financial crisis, falling interest costs and greater leverage have accounted for nearly one-fifth of an overall 8.8 percentage points increase in the return on equity (ROE) of S&P 500 firms. The risk of rates now being higher for longer could prevent firms from taking on more leverage, hitting long-term profitability, the strategists added.

Might be a good time to check in on the capital structure of companies in your portfolio.

That Was Fast

Yesterday we talked a little bit about the collapse of Evergrande (more on them shortly). Today, Country Garden, the largest property developer in the country, announced that it is expecting to default on its bond payments.

As the Wall Street Journal reports:

Country Garden said its sales have come under “remarkable pressure,” which worsened its problems. The developer’s contracted sales in the first three quarters of this year dropped 44% from a year earlier to the equivalent of about $21 billion. The drop was particularly steep in September, when Country Garden’s sales plummeted 81% to just $846 million, it said in a regulatory filing.

Not good! Especially not good for the country as a whole given the fact that the OECD, in June of this year, estimated that the Chinese economy would grow by 5.4% in 2023. Given that Chinese property purchases require down payments of 60-90% of the purchase price according to the East Asia Forum, the sudden evaporation of sales means that the Chinese consumer may be substantially more pressured than previously thought.

Oh, and then there’s this, also from the East Asia Forum:

There are also structural pressures on Chinese growth. Not least among them are regulatory actions that severely dampened business confidence, especially among technology companies and foreign-invested enterprises.

This snippet from an article published just yesterday seems remarkably prescient given an article that appeared in Bloomberg today that Evergrande has just plunged its creditors into fresh uncertainty with a rug-pull on its restructuring plan after the company failed to gain regulatory approval.

If you want to understand why all of this could eventually matter to you and I, read this.

Final Thoughts…

Yet another Chinese business tycoon is AWOL. European stocks are feeling it. Higher rates for longer are a good thing. Boeing isn’t making very many 737 MAXs. You don’t have to wait till tax time to claim your EV credit. Living to 120 may be a thing soon.