Idea Roundup #11

The turnaround at PayPal is underway, a little humble pie, and more.

Thanks for reading this week’s investment roundup! As always, everything here is opinion and nothing is investment advice. Please read the disclosure below for more. Enjoy!

1. PayPal PYPL 0.00%↑

I’ve discussed PayPal a few times over the years over at Seeking Alpha (you can read some of those pieces here and here), and for the most part I would categorize my bullish outlook on the stock as… early, which is finance jargon you use when your idea has either A) cratered or B) has gone nowhere. Thankfully, option B is largely the course the stock has taken. Today, though, there are reasons to think that the payment provider is finally turning things around.

First off, the last six months (well, three months, really) have seen PayPal’s stock surge 17%, reflecting some renewed optimism around the company’s new leadership (of whom I am a big fan) and rumblings from the company on conference calls and at investment conferences that the company will begin to utilize purchase data to create a better ROI for advertisers.

Now, I hear you. As a consumer, nobody wants that. But as a shareholder… well, that’s perhaps a different story.

I also would point out that PayPal is trading at a considerable discount to the rest of the S&P 500 SPY 0.00%↑.

I, for one, think this gap is important, and—given the fact that there is no real material threat to PayPal (i.e., it’s not going bankrupt) that I’m aware of, I think it is more likely to close than widen further.

Those skeptical of PayPal may still have clouded thoughts given the payment processor’s once-lofty valuations not that long ago, and that’s fair. However, it does seem to be a new day at PayPal, and I think the stock is interesting at these levels.

PYPL 0.00%↑ Take: Bullish

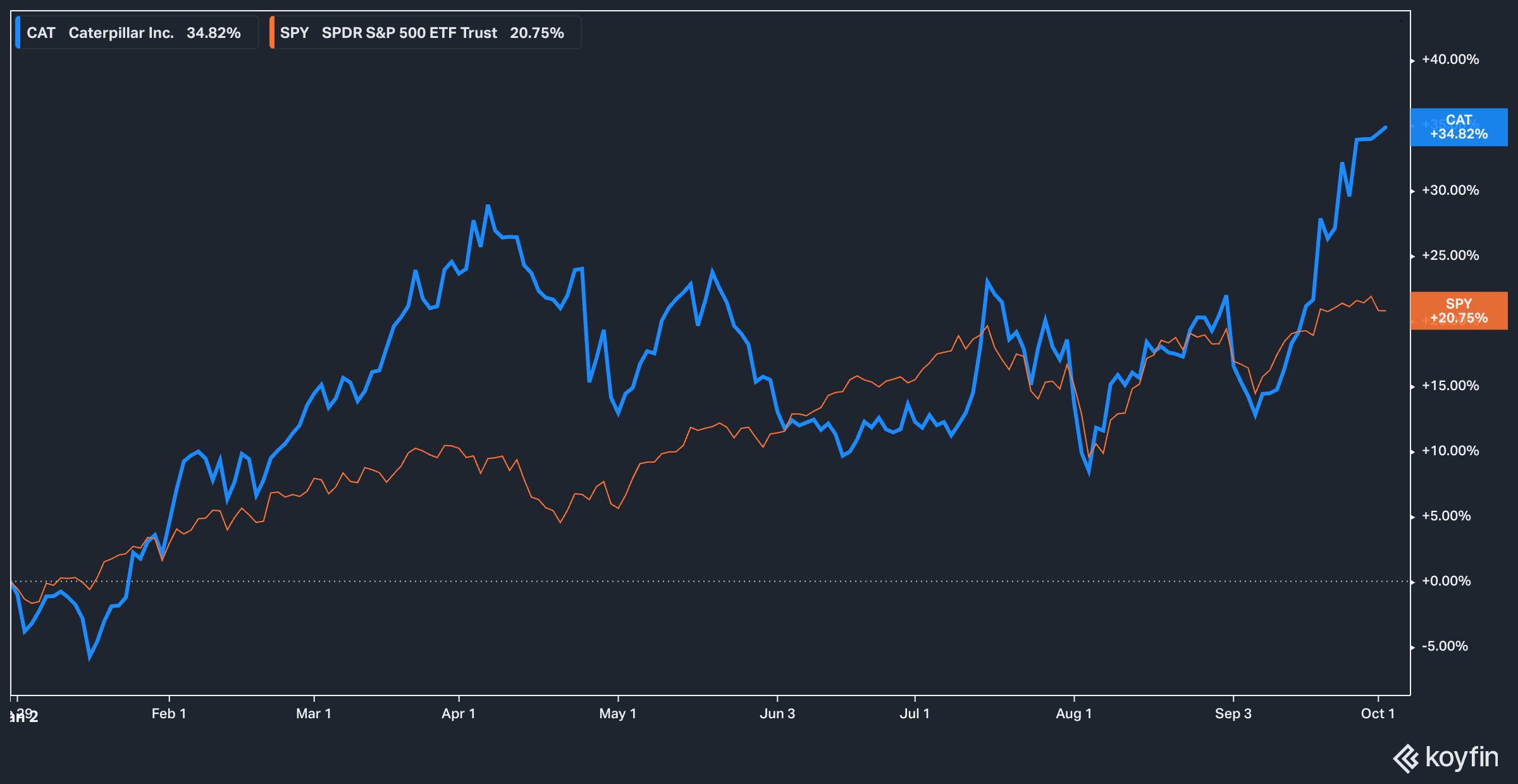

2. Caterpillar CAT 0.00%↑

Caterpillar has quietly had itself a year. The heavy equipment manufacturer has defied the expectations of many (myself included) in that the company has navigated the high interest rate environment quite well.

The most recent mini-rally in the stock has been driven by the Fed’s cutting interest rates, but even prior to that the stock was no slouch in 2024.

I think that Caterpillar’s success is mostly a story of competent management. It’s impressive to see that over the last three years—while forward-looking revenue expectations have fallen, no less—the company has consistently managed to find efficiencies and raise its growth and operating margins.

A recent Barron’s article acknowledged this as well and pointed out that the company has also done a great job preparing its mining segment for an expected international rebound.

CAT 0.00%↑ Take: Bullish

3. Palantir PLTR 0.00%↑

Oh boy. Here we go.

I’ve beaten the drum on Palantir for a while now. What have I gotten for it? Well, my teeth have more or less been kicked in.

Some would say it’s time to change course, that enough damage has been done and clearly—clearly!—the broader market doesn’t agree with you.

While it may be true that the market doesn’t agree with me now on Palantir (to put it lightly), I still think there are reasons to be suspicious about the long-term viability of this company. Here’s just one:

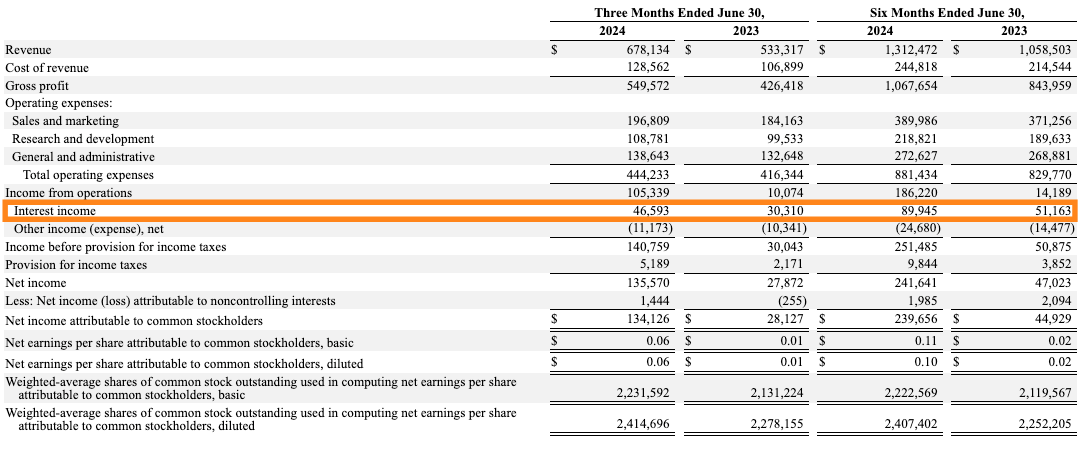

With the last couple of quarters excluded, Palantir has gotten quite a boost from interest income over the last several years with higher interest rates. The company had a mountain of cash, and when interest rates rose it moved that cash into income-generating bonds.

As you can see, Palantir generated $251 million in income before taxes for the six months ending June 1st, 2024. Of that amount, $89 million—roughly 35%!—came from interest income.

You may have heard that the Fed did a little interest-rate lowering last week, and most of the voting members of the FOMC believe that more interest rate cuts will be coming in the future. Therefore, it can be reasonably expected that this additional bit of income that squeezes through to the bottom line may no longer be as robust as it was.

Now, that doesn’t mean what it used to mean for Palantir—back when the company struggled to turn a profit and, arguably, interest income is what pushed them over the line. But it does eat into net profit margin at the end of the day.

There are other reasons, but it would take longer to get into than the Idea Roundup format suggests. I may do a deeper dive on Palantir in the coming weeks, because there are many other things I see that, in my view, are cause for concern. In the meantime, I will quietly eat my humble pie as investors continue to pile into the stock.

PLTR 0.00%↑ Take: Bearish

While you’re here, check out my latest writeup on Starbucks SBUX 0.00%↑

4. REV Group, Inc REVG 0.00%↑

Let’s change gears here and head over to small-cap land and REV Group, a maker of emergency vehicles (firetrucks, ambulances), recreational vehicles, and commercial vehicles like transit and school buses.

The company recently experienced a setback when suffered its first top-line sales miss in 8 quarters, sending the stock down 11% in one day.

While the company faced difficult comps in this quarter, the miss was still disappointing. However, I think there’s reason to be optimistic here that conditions will improve. The company’s RV segment (which is, admittedly, my least favorite part of this business) has at least falling interest rates going for it. As long as the economy avoids a wider recession, lower financing rates are likely to be a boon for industries like this as they have been in the past.

Further, despite disappointing top-line performance, management has been able to ensure efficiency across the board. The company’s forward EBIT and EBITDA expectations have continued to move upward.

Overall, the situation looks interesting to me and may be worth a deeper dive.

REVG 0.00%↑ Take: Tentatively Bullish

In Other News…

wrote a great piece on Nike NKE 0.00%↑ back in July, which seems especially prescient given the latest weak earnings from the company. over at Invarient recently published an informative and brief deep dive into the tobacco industry (covering MO 0.00%↑ and PM 0.00%↑, among others) in Podcast form, and, I would say, it’s worth a listen. put out a great (and free) wide-ranging piece on unit economics, understanding payment terms, burn multiples, and more. Definitely worth a click. Disclaimer: The content in this article is for informational, educational, and entertainment purposes only. This content is not investment advice, and individuals should conduct their own due diligence before investing. The author is not suggesting any investment recommendations—buy, sell, or otherwise. This article is not an investment research report but a reflection of the author’s opinion and own investment decisions based on the author’s best judgement at the time of writing and are subject to change without notice. The author does not provide personal or individualized investment advice or information tailored to the needs of any particular reader. Readers are responsible for their own investment decisions and should consult with their financial advisor before making any investment decisions. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned. Any projections, market outlooks, or estimates herein are forward-looking statements based upon certain assumptions that should not be construed as indicative of actual events that will occur. Any analysis presented is based on incomplete information, and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. The author expressly disclaims all liability for errors and omissions in the service and for the use or interpretation by others of information contained herein.