Idea Roundup #4

"Hi... I'm in Delaware" -- Wayne Campbell (and Elon Musk, probably). This week's roundup includes thoughts on Snowflake, Tesla, and more!

Welcome to another Idea Roundup! Before we begin, some housekeeping… as you may have noticed, I’ve recently changed the name of the newsletter from The Market Beat to Ironside Equity Research.

The reason for the switch is fairly straightforward—first, there are plenty of publications out there with some variation of Market Beat in the title. Second, I think Ironside Equity Research more readily conveys what this newsletter is more or less about, which is writing about stocks (and occasional commentary).

Thank you for your support and continued readership! Now, let’s get to the ideas…

1. Snowflake (SNOW) SNOW 0.00%↑

A lot of companies make promises about utilizing AI in new and interesting ways, but these promises often, well, fall short of investor expectations (I.e., they don’t make any money). Investors would be forgiven for harboring a dash of skepticism, then, about Snowflake’s recent push to become the go-to company for AI development.

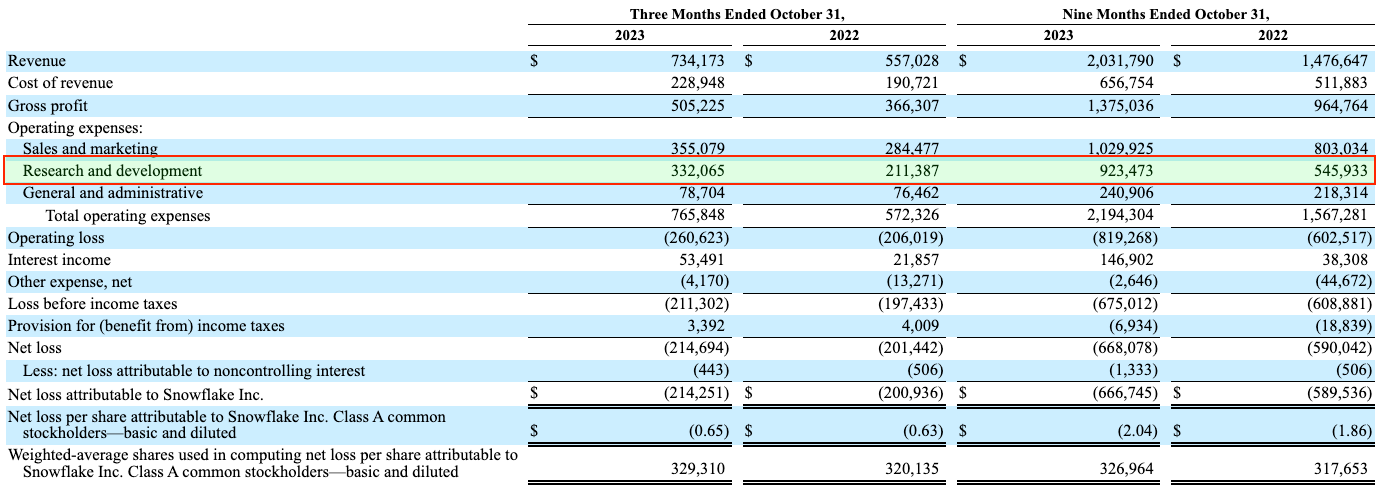

R&D spending at the company has skyrocketed year over year, exceeding revenue growth.

Now, there are a lot of ways to go here: it’s a very heartening thing to see companies take a big risk and spend on R&D for benefits that may come at some point down the road, but this would usually be interpreted as a good thing when the company in question is profitable, which, as you can see from the chart above, Snowflake isn’t.

Further muddying the waters is the fact that Snowflake is a capital-O offender of one of my pet peeves of tech stocks: the company engages in unbelievable amounts of stock-based compensation. For the nine months ending October 31st, Snowflake incurred $862 million of SBC expense. This figure is, essentially, what keeps the company from GAAP profitability.

Again, kind of a tough one: promising R&D spending on the one hand which indicates a willingness of management to go out on a limb, but a whoooole lot of dilutive action going on behind the scenes for investors.

2. Paramount Global (PARA) PARA 0.00%↑

The Great Streaming Wars were brutal,1 but as with prior contests in the ever-evolving media and entertainment landscape, there’s always a deal to be found in the wreckage. Paramount has top-notch IP (even if doesn’t exactly match, say, Disney’s DIS 0.00%↑), and, if reports are to be believed, the stock could soon be out of the hands of the Redstone family—Brian Allen has submitted at $14 billion buyout offer at $28.58 per share (as of this writing the stock trades at $14.84).

Long-suffering Paramount shareholders would almost certainly rejoice if the deal were to close since the hits have just kept coming for the company (the stock is down more than 30% over the last year).

The story of Allen’s buyout offer broke only this morning, so this will be one to keep an eye on going forward.

3. Tractor Supply Co (TSCO) TSCO 0.00%↑

Tractor Supply is a much-beloved nationwide chain that specializes in “rural lifestyle retail.” The company operates 2,393 stores as of the latest available quarterly data across 49 states. The company is set to report earnings next week.

I have covered Tractor Supply over at Seeking Alpha before, and I am generally bullish on the chain’s outlook (the market doesn’t seem to agree with me, however, since the stock has essentially traded sideways for the last year.

With that in mind, Tractor Supply seems to be (in my mind) a play worth a look for investors with a 3-year plus time horizon: the outlook for the company is favorable, and management is stellar.

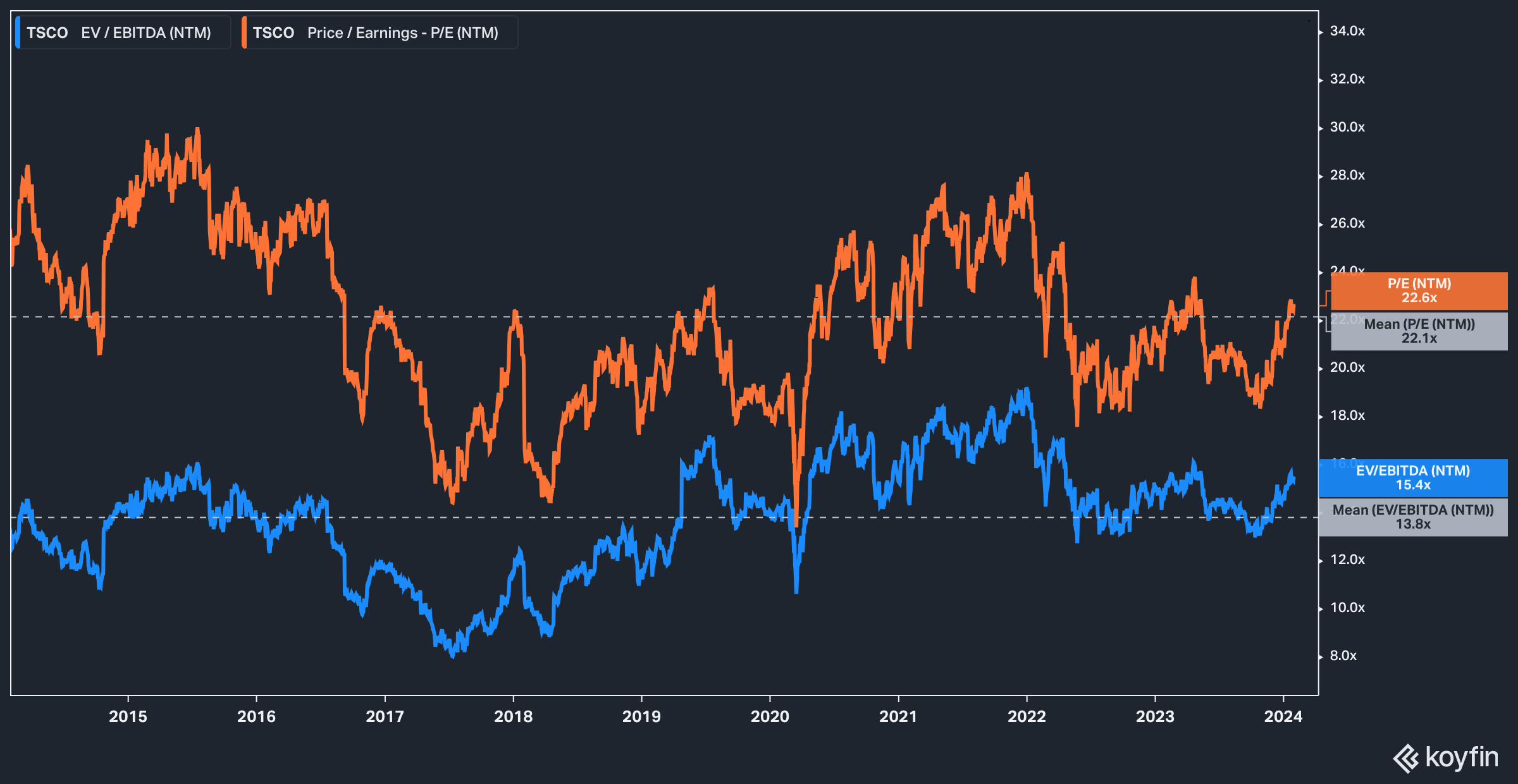

Valuations have been more or less sideways as well for the last several years.

Retail is a tough business with great execution being a key differentiator (just look at Costco COST 0.00%↑). Tractor Supply has excellent merchandising and strong customer loyalty—I’ll be watching the upcoming earnings closely.

4. Tesla (TSLA) TSLA 0.00%↑

A note of caution—there’s a whole lot of speculation that’s gonna go on with this one.

Yesterday a Delware Chancery court invalidated Elon Musk’s 2018 compensation package, worth roughly $55 billion. Tesla stock hasn’t really budged much today on the news (since the ruling will certainly be appealed), but the risk of owning Tesla stock has nonetheless gone up considerably in the last 24 hours.

The comp deal involves 12 tranches of options, all of which have vested but which have not been exercised, which might not sound so risky on the surface except for the fact that Musk has already pledged a significant amount of shares to cover personal indebtedness related to his buyout of Twitter.

Given the fact that 303 million of the 715 million shares owned by Musk are now in jeopardy, Musk now runs the risk of being out of compliance with the company’s stock pledging guidelines that cap Musk’s stock pledging to 25%. While it’s unclear what the outcome here would be (given the fact that the board has been more than accommodating for Musk over the years), the long-running narrative that Musk has too much on his hands to properly run Tesla is unlikely to go away any time soon.

For most ardent Tesla fanboys all of this is just likely to be viewed as vindictive retribution against Musk by an establishment that hates him, rather than run-of-the-mill compliance oversight brought upon the company by a shareholder who disagreed with a pay package they deemed excessive, so it seems unlikely that a wave of retail selling is imminent. The real (yet unanswered) question is what will Musk be forced to do with his shares.

No matter where you stand on Tesla, however, nobody can ever accuse the stock of company of being boring.

If you haven’t already, check out this stock deep-dive from November 2023!

Why We Think This Small Cap Stock Could Have 70% Upside

Thanks for checking out the latest equity deep dive from Ironside Research! If you enjoy our work, please be sure to subscribe to receive updates when we publish new research. Also be sure to check out our disclaimer below. Cheers! Highlights Carriage Services is a cemetery and funeral operator

Disclaimer: The content in this article is for informational, educational, and entertainment purposes only. This content is not investment advice and individuals should conduct their own due diligence before investing. The author is not suggesting any investment recommendations—buy, sell, or otherwise. This article is not an investment research report but a reflection of the author’s opinion and own investment decisions based on the author’s best judgement at the time of writing and are subject to change without notice. The author does not provide personal or individualized investment advice or information tailored to the needs of any particular reader. Readers are responsible for their own investment decisions and should consult with their financial advisor before making any investment decisions. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned. Any projections, market outlooks, or estimates herein are forward looking statements based upon certain assumptions that should not be construed as indicative of actual events that will occur. Any analysis presented is based on incomplete information, and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. The author expressly disclaims all liability for errors and omissions in the service and for the use or interpretation by others of information contained herein.

C’mon. It’s over. Netflix NFLX 0.00%↑ has won. Let’s call it a day.