The Real Estate Gurus Were Lucky, Not Right.

Plus, Another Day, Another Interest Rate story

Womp Womp

Working from home has impacted a whole lot of industries, but none more obviously so than the commercial real estate sector. This sector is most broadly defined as any real estate owned for income generating, investment, or business purposes. In other words, any real estate not personally owned and lived in.1

Now, there once was a time not that long ago when financial-guru-slash-charlatans would actively advocate for people to dump their life savings into real estate as ‘the best investment possible’ for mom-and-pop types. We all know that only good things can happen when regular people utilize ridiculous amounts of leverage to acquire assets, right? Right?

Anyway, what the invest-in-real-estate gurus always tended to ignore was the fact that for the last forty or so years, almost everything possible was moving in favor of the housing market. Globalization and the ever-increasing efficiency of the home building industry meant that homes could be built more cheaply than ever before. A multi-decade decline in interest rates meant that money was cheap, and so people could afford more home than ever before. People also continually refi’d their mortgages as interest rates fell, creating yet more hype around how easy it was to generate a lower payment or extract cash from the asset (the house) to buy another one.

All of this was great, and people made a lot of money (or some did, a la the greater fool game in house flipping), while a lot of people ended up saddled with a bunch of debt and suddenly realizing that having a 90% LTV on a rental property meant that virtually all of that rent never made it into their personal bank account.

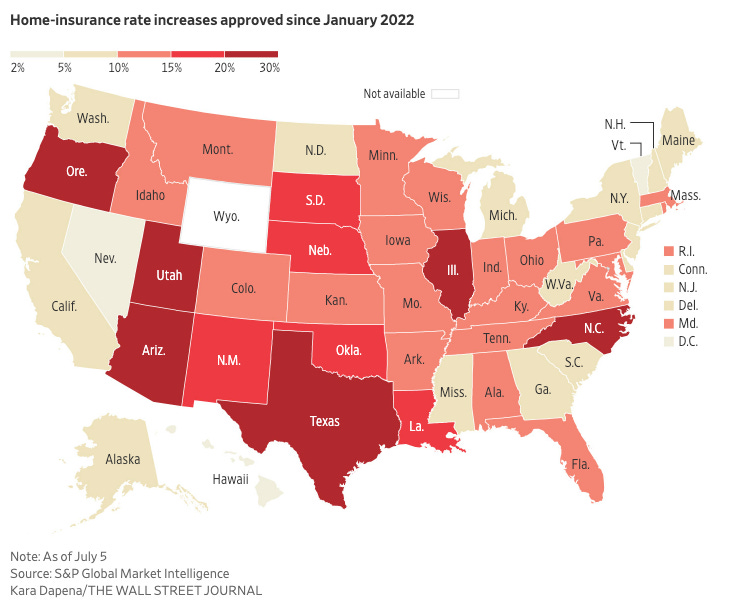

Of course, interest rates going up is not news—I talk about it a lot here. But what is interesting about the real estate market is that a new dragon to slay has emerged, one that is threatening to upend mom-and-pop investment home owners and big, institutional owners of commercial real estate alike: rising insurance costs.

Insurance costs and claims have been rising at a rapid clip, forcing insurers to exit certain geographies altogether (Florida, California, Louisiana), to restrict coverages offered, and ramp up premiums.

The culprit in this case isn’t just extreme weather events causing mass damage, but the snarled supply chain and the availability of labor, which makes getting the repair materials and the workers to complete the repairs more costly.

The Wall Street Journal reports:

While insurance premiums are rising virtually everywhere and for all building types, some cities have been particularly hard hit, especially for multifamily buildings. Costs to insure rental-apartment buildings rose 14.4% annually on average in Dallas, 13% in Los Angeles and 12.6% in Houston. Some owners struggle to find anyone willing to insure their buildings, Moody’s said.

“I have never seen such a significant and rapid change in insurance capacity as well as spikes in pricing,” said Alexandra Glickman, leader of the real estate and hospitality practice at insurance consulting firm Gallagher.

For some property owners, the impact of rising insurance costs has been more punishing than rising interest rates. Many landlords still have low debt costs because they signed long-term, fixed-rate mortgages before 2022 that don’t expire for years to come. But insurance contracts typically renew every year. That means virtually every property owner has been forced to either sign a new policy at a higher cost, or skip insurance altogether.

You know, there have been very few silver linings over the last three or four years in my mind, between COVID, rising inflation, etc. However, I have to say I can take a little bit of comfort in seeing the faux-gurus of real estate evangelism eat their words as they slowly discover that they were not right, just lucky.2

Another Day, Another Interest Rate Story

Something I’ve been thinking about for a while is how incredibly resilient the U.S. economy has been overall throughout COVID and the pandemic. Of course, I’m not alone. The continued ability to spend cash demonstrated by the American consumer has confounded virtually every economist out there.

And yet, in terms of the purchase cycle for long-lived household assets (washers & dryers, cars, etc), it kind of isn’t that surprising. The proverbial tide, however, may be about to come in.

This article from the Wall Street Journal outlined how consumers are starting to finally pull back from major purchases and balking at just how much things cost nowadays.

Buying a home or car right now is “completely unaffordable for the typical American household because you’re mixing the higher borrowing costs with the high prices,” said Mark Zandi, chief economist at Moody’s Analytics.

He estimates that the typical American household would need to use 42 weeks of income to buy a new car, as of August, up from 33 weeks three years ago. The National Association of Realtors calculates that the typical American family can’t afford to buy a median-priced home.

Also:

But some with lots of credit-card debt are feeling particularly strained. “Consumers are carrying much higher balances than they were two years ago,” said Charlie Wise, head of global research and consulting at TransUnion. “There are always people at the margin where any increase in rates is going to hurt them.”

The typical credit card carried a 20.7% interest rate in May, up from 14.6% in February 2022, according to the Fed. Americans’ collective credit-card debt just passed the $1 trillion mark for the first time.

Readers will remember that we discussed the fact that Americans have collectively crossed the $1 trillion mark for credit card debt just last week.

Final Thoughts…

America’s responsible lawmakers continue to threaten to shut down the government. Scientists are getting closer to achieving longer life for humans. Jamie Dimon thinks rates could hit 7%. JP Morgan settles the Epstein stuff. Ruh-roh: Glencore traded Russian copper via Turkey. How a four-day work week actually gets accomplished.

Thanks for reading! As always, please consider sharing this email with a friend who might enjoy it. Cheers!

Yes, it is far more granular than that and could be more precisely defined, I know. Get off my back.

I wish I could guarantee they would have to eat their words, but unfortunately they probably won’t. There are plenty of rubes out there always ready to shill out big money for courses and online seminars with pie-in-the-sky prices. C’est la vie.

Great insights!!! Thank you for sharing.