This Self-Funding Small Cap Company Has Huge Upside Potential

Diving into Franklin Covey, a corporate training company with a robust and unique suite of offerings.

Background

Today we focus on a small-cap company that has, in my opinion, a lot of greenfield in front of it: Franklin Covey Co. (FC) FC 0.00%↑. Here are some of the highlights—

Price: $42.63

Market Capitalization: $556 million

TTM Revenues: $279.5 million

Short interest: 4.3%

Shares outstanding: 13.29 million

Industry: Professional Services

Trailing EPS: $1.29

Average 30-day volume: 89,880

You probably already know Franklin-Covey at least in passing due to the book The Seven Habits of Highly Effective People by Stephen R. Covey. Covey passed away in 2012, but his book (and subsequent books like First Things First) has been massively popular since its publication in 1989.

In past years the company was largely known for its retail, individualistic approach. The company made and sold various planners and at one point even operated retail locations where folks could go and purchase Franklin-Covey products, calendar refills, books and courses, and the like.

Today, however, the company is considerably different—and while the lessons from Seven Habits remain an integral part of the company, the focus has shifted to enterprise and conducting training and coaching on company culture, leadership, building trust, and developing unified execution.

In the past, these corporate offerings were a la carte. Clients would pay for an individual course or seminar, employees would attend, and that would pretty much be it. This was not effective for several reasons: the short duration of the training made it difficult to implement lasting outcomes. Attendees fell behind on work while engaged in an immersive, multi-day seminar. Perhaps most importantly, it was difficult to engage a company at scale when conducting this sort of one-off training.

This changed around 2016 when the company altered its offerings from a la carte to what was dubbed the ‘All Access Pass’ (AAP going forward). Under the AAP model, clients would:

Gain access to the full library of Franklin Covey resources and training

Be able to access content via live online classes, on-demand classes, or in-person

Pay on a subscription/contract basis vs. one-and-done payments

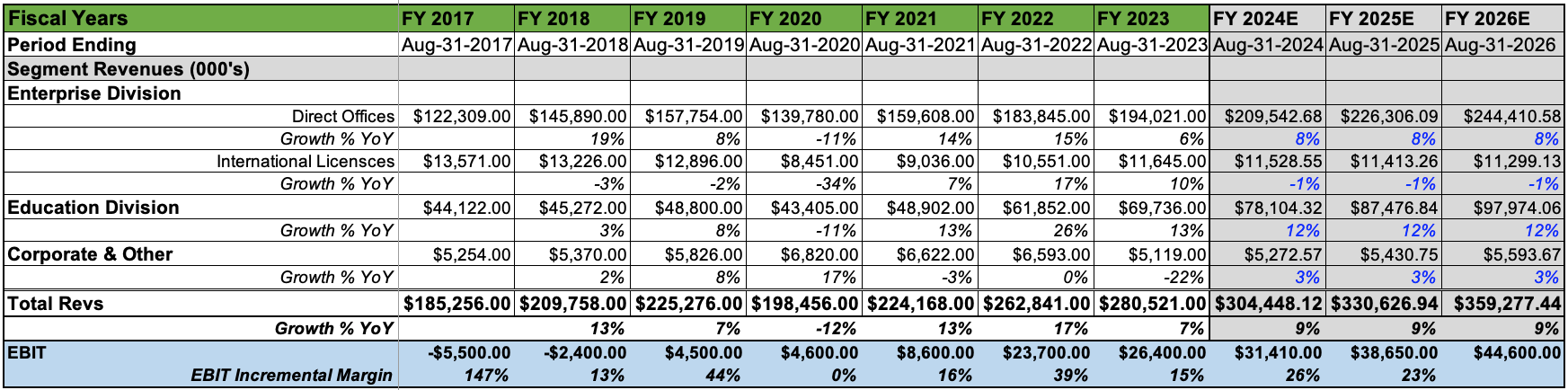

In 2021 Franklin Covey named Paul Walker as its CEO. An inside hire, Walker has been with Franklin Covey since 2000 and worked his way up through the management ranks. While serving as COO, the company made an important acquisition with Strive, a startup content-delivery provider, which enhanced the company’s online training offerings. This side of the business is the Enterprise Division, which brought in $194 million in revenues for FY2023 compared with $183 million in FY2022. Competitors for this division include Korn Ferry (KFY) KFY 0.00%↑, Udemy Learning (UDMY) UDMY 0.00%↑, and LinkedIn Learning to name a few.

In addition to corporate offerings, Franklin Covey also has a fast-growing K-12 education business. Known as the ‘Leader In Me’ program (LIM going forward), the company currently partners with over 7,000 schools to deliver leadership-oriented training to school and school district employees, as well as students.

The education push began in 2008, led by Stephen R. Covey and his son, Sean Covey (who still oversees the program). Over the last decade the segment has delivered remarkable growth, brining in $69 million in sales for FY2023 compared with $61 million for FY2022.

The company also has two other segments, International Licensees and Corporate & Other, but these are much smaller business units, accounting for ~4% and ~2% of FY2023 sales, respectively.

Franklin Covey’s revenues are, in my assessment, high quality. Unlike a traditional subscription model, clients don’t pay Franklin Covey month-to-month or quarter-to-quarter. Instead, contracts are paid up front in cash, and Franklin Covey recognizes the revenue throughout the life of the contract. Walked outlined some of the key components of the company’s contract model in the company’s latest earnings call:

With upfront invoicing, working capital is actually a source of cash for us. Subscription contracts are built at the start of the contract term, and cash is collected long before the subscription contract's full revenue is realized. Multiyear contracts are generally billed one year in advance and are noncancelable, and the timing of collections and cash outflows is a durable aspect of our business model.

The two main points for me are the non-cancellable aspect of the contracts, and the fact that many of those contracts are multiyear. In fact, a majority of Franklin Covey’s clients are now on multiyear contracts—54% in the latest quarter, up from 48% year-over-year.

Additionally, the addressable market for corporate training is very, very large. In its latest 10K, Franklin Covey quotes a statistic from Training magazine that the TAM for the training industry sits at roughly $101 billion.

Deployment Of Capital

As you might imagine, Franklin Covey’s business is not very capital intensive and has many ‘flywheel’ characteristics that allow margins to expand as revenues grow. Capital expenditures as a percentage of revenues have averaged just 1.93% over the last 10 years.

Company leadership has also dedicated to returning cash to shareholders in the form of share repurchases. Over the last 10 years, shares outstanding at Franklin Covey have fallen by 20%, and management expects to return “substantial portions” of FY24 cash flows to continued repurchases.

In a bit that is music to my ears, Walker outlined the company’s rationale for the aggressive repurchases in the last earnings call:

Why do we have such high conviction in repurchasing our stock, something we know is shared by many of you as well. Two simple reasons. First, because we have high confidence in the market opportunity before us and our ability to execute it. And second, because we believe repurchasing our stock even at significantly higher than current prices has a very compelling investment thesis. That being first that we believe that we are and would be purchasing shares at a significant discount relative to the net present value of our expected cash flows.

As just noted, we believe that both our recent purchases and our purchases over the years reflect this. And because we believe that a much smaller than typical percent of the net present value of our company's cash flows is attributable to reliance on the residual exit value of these cash flows. Because, one, purchasing shares at or near our current market cap provides a high free cash flow yield, and we expect free cash flow to grow substantially in the coming years. The combination of these factors gives us confidence in investing excess cash flow in the business and in share repurchases can generate significant additional value for shareholders in the coming years.

Something I’ll be keeping an eye out for is any announcement of a new stock repurchase plan from the Franklin Covey board—of the February 2023 $50 million repurchase plan, only $9.7 million remains authorized for repurchases as of November 2023.

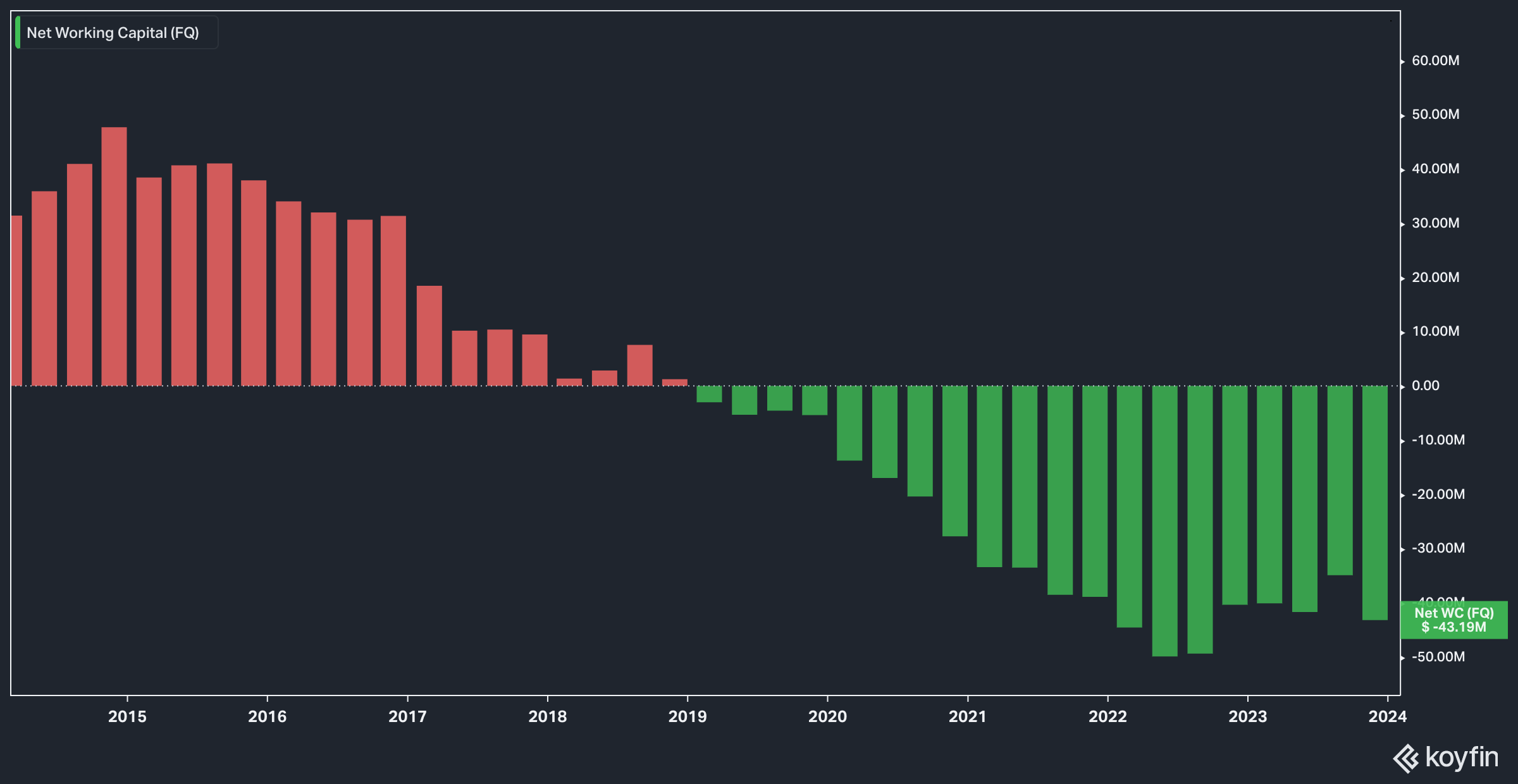

It’s not difficult for management to justify dedicating such a large portion of cash flows to repurchases when you have a balance sheet like Franklin Covey’s. The vast majority of the company’s current liabilities stems from deferred subscription revenue, which is simply cash from clients waiting to be recognized as revenue, and long term notes payable less current portions stood at just $1.5 million in the latest quarter.

The company boasts a negative net debt of -$20.7 million on an LTM basis and a debt/capital of 17%.

Performance & Estimates

The last year has been disappointing for Franklin Covey.

The stock has posted a one-year total return of roughly -6%, while the Russell 2000 (RTY) eked out a ~5% return. The five-year total return has been better, with Franklin Covey delivering a 71% return against RTY’s 36%, but as of lately the narrative seems to be that the stock is in the doldrums.

Part of this has to do with the fact that quarterly earnings have fallen on percentage growth basis year-over-year:

After lapping easy 2021 comps, Franklin Covey has run into the same post-Covid growth hangover that has affected so many companies as of late. Easy comp laps in 2021 and strong growth in 2022 has created an environment where anything less than knocking it out of the park is likely to be perceived as a letdown.

I want to note, however, that over a ten-year period (seen above), the quarters of underperformance on comps have generally led to outperformance, to which the stock has reacted favorably in the past.

Now, let’s discuss segment results and projections.

In the big picture, I expect that base-case growth for Franklin Covey to be at 9% up to FY26. This thinking reflects assumptions that Education growth will continue to outperform, while Enterprise revenue growth will normalize to ~8%.

More granularly, the big pole in the tent for Franklin Covey is the Direct Offices unit of its Enterprise Division, which saw 6% revenue growth in FY23, down from 15% in FY22 and 14% in FY21. While earnings for this segment have previously been in the teens, I believe 8% to be a very achievable base case for Franklin Covey.

My base case also expects International Licensees and Corporate & Other Income to be down to flattish over the next three years. Given the small overall impact these units have on Franklin Covey’s overall performance, a shrinking International Licensees business shouldn’t greatly impact the company’s overall performance over the next three years.

The big question mark—and a key driver of growth—is the continued expansion of the company’s Education offerings. This segment has delivered impressive growth year over year, and boasts a 5-year revenue CAGR of 7.4%, well above the Direct Offices revenue CAGR of 4.2%.

This continued growth in education Education is also quite important to the economies of scale for Franklin Covey, as evidenced by my estimate of incremental EBIT margin rising from 15% in FY23 to the mid-to-low 20% range for FY24 and FY25.

Reverse DCF & Valuation

The market, for its part, seems to be pricing the stock today roughly around my base case assumptions. Running a reverse discount cash flow allows us to estimate what assumptions the market may be making about a stock—in other words, what’s currently baked in.1

However, we almost immediately we run into the limitations of the reverse DCF when we attempt to assess Franklin Covey’s WACC. 8% is a moderate estimate in my view, given current interest rates, but as described above, WACC plays very little into Franklin Covey’s day-to-day business. The company run on virtually no debt and is self funding with a negative working capital structure.

Therefore, I tend to think that the 8% growth implied in the reverse DCF tends to skew conservative for a base case. Additional assumptions made in my reverse DCF were a long-term growth rate of 1% (again, conservative from my view), and a tax rate of 23%.

From a valuation perspective, Franklin Covey has never been cheaper.

Over the last three years the stock has fallen from trading a mind-boggling (and mystifying) 160x forward earnings estimates to a quite reasonable 18.6x next year’s estimated earnings. NTM EV/EBITDA estimates are also lower than the 10-year average of 15x, trading today at 9.6x.

Other metrics also reveal the current attractive valuation for the company:

As you might expect from a company with de minimis debt, an aggressive share repurchase program, and a negative working capital structure, Franklin Covey has posted impressive returns on capital since 2021.

ROC figures in the-mid teens are impressive, but again not surprising. Again, reference the chart of Franklin Covey’s working capital above, which turned negative in 2019—it didn’t take long for returns on capital to jump significantly following that crossover.

Bear, Base, & Bull Cases

Below are my basic assumptions for a Bear, Base, and Bull cases for Franklin Covey through FY2025.

For the base case, EPS of $2.40 is actually below the average analyst consensus estimate of $2.65, which I have set as my Bull case. The rationale behind this is relatively straightforward—achieving $2.65 implies a range of scenarios coming to pass (continued large scale repurchases of stock, greater incremental margins and economies of scale, net income margin expansion, etc), and it seems to me that the few analysts who cover Franklin Covey are perhaps a little out ahead of themselves.

The Bear case for Franklin Covey, in my opinion, largely rests on growth in the Education segment stalling out, which as of this writing there is very little indication of that happening.

My base case includes a 24x earnings multiple, which is above today’s levels but not unprecedented since the stock spend the majority of CY2023 trading in this range.

I would not fault someone for believing that even Base case EPS seems very optimistic, but it seems to me that more is working in Franklin Covey’s favor than against it. CEOs are clamoring more and more for ways to improve employee cohesion and maintain a healthy corporate culture in remote or hybrid work environments, which plays perfectly into Franklin Covey’s suite of on-demand offerings. Combine this with the now self-funding nature of the business, and Franklin Covey appears to have many of the attributes of a potential multi-bagger in the long term.

Disclaimer: The content in this article is for informational, educational, and entertainment purposes only. This content is not investment advice and individuals should conduct their own due diligence before investing. The author is not suggesting any investment recommendations—buy, sell, or otherwise. This article is not an investment research report but a reflection of the author’s opinion and own investment decisions based on the author’s best judgement at the time of writing and are subject to change without notice. The author does not provide personal or individualized investment advice or information tailored to the needs of any particular reader. Readers are responsible for their own investment decisions and should consult with their financial advisor before making any investment decisions. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned. Any projections, market outlooks, or estimates herein are forward looking statements based upon certain assumptions that should not be construed as indicative of actual events that will occur. Any analysis presented is based on incomplete information, and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. The author expressly disclaims all liability for errors and omissions in the service and for the use or interpretation by others of information contained herein.

Reverse DCFs, like traditional DCFs are heavily (heavily!) reliant on assumptions. This is an additional reminder to treat estimates with a grain of sale, and that nothing here is investment advice.

Hi Steve,

I read your analysis on FC again. It's a very succinct piece. Thank you.

I don't understand/appreciate the product offering enough to dive further. It's a personal choice. I prefer owning businesses with mission-critical offerings (Veeva, Wisetech, VAT..) or having mediocre alternatives (Willscot, MIPS, FND). Additionally, I prefer businesses with more abundant growth opportunities. If the company could find a new way to leverage its knowledge/courses or acquire similar businesses, then I'd be more interested. Right now, it seems the only cap allocation option to create value is to buy back shares....however, that's short-term and doesn't change the business fundamentally, IMHO. Again, it's a personal choice.

Thanks for your work again. Trung - Sleep Well Investments

Thanks for the write up. I agree the revenue is high quality from a working capital dynamic. A key question with this company is whether they have an effective sales organization and go to market. Relatedly, are customers receiving excess value from the all access pass? Would customers from one division of a large company ever refer all access pass to their colleagues in another division? If FC can get their net revenue retention numbers to inch closer to Gartner's, this could be a be a great stock to own.